| Medtecs International is the only Singapore-listed producer of personal protective equipment (PPE), a business that has been critical in the fight against Covid-19. As its factories in China, Cambodia and the Philippines ramp up production of PPE for global markets including Europe and the US, profits and cashflow have turned into an unprecedentedly large incoming tide for Medtecs. Based on its guidance in 3Q results announcement, Medtecs will record at least US$130 million in net profit for FY20. In comparison, it was just US$1.2 million in FY2019. See how the 2020 quarters add up:

Given the fast-evolving business environment in 2020, Medtecs gave its first guidance on 5 May 2020: It said it “expects revenue and profit growth in the second quarter to exceed that of 1Q 2020”. It proved to be an incredible understatement. 2Q20 profit turned out to be US$35 million, far exceeding the $3.7 million recorded in 1Q20. DBS Group, which is the only house covering Medtecs currently, has opted to be conservative about its 2020 forecast. In its initiation coverage on 8 Dec 2020, DBS forecasted US$130 million -- in other words, exactly the minimum based on Medtecs' 13 Oct 2020 guidance. This opens the door wide open for DBS to upgrade its target price after the actual higher profit is announced. Consider also the arguably low valuation of Medtecs. Based on the US$130 million profit forecast, which is 31.6 Singapore cents EPS, the stock's PE ratio is 3.5X on a recent stock price of $1.12. Is the market overly worried about the sustainability of the exceptional business environment in 2020 for Medtecs? |

||||||||||||||||||||

It doesn't help that DBS is the only one providing coverage, so Medtecs needs time to gain more significant traction among Singapore investors.

Being the only listed PPE producer in Singapore has added to that challenge as has the fact that Medtecs has been virtually non-existent on the radar of Singapore investors pre-Covid.

Its 4Q2020 results, likely to be announced in weeks to come, could lend a sparkle to the market's view.

Greater positivity could materialise if Medtecs will once again provide guidance on its revenue and profit for the near term.

More critically, Medtecs will need to highlight that its business fundamentals have been strengthened for good by Covid-19.

DBS' 21-page initiation report did delve into that, as the following excerpts show:

| 1. Steady customer relationships a bedrock for Manufacturing segment. |

MED has been a long-time supplier for customers such as Premier Inc. and the governments of Taiwan and Singapore. We believe this relationship bodes well for the Group, enabling MED to remain a choice supplier even after COVID-19. The Group had sacrificed higher sales of Medtecs branded products to meet the needs of these customers during COVID-19.

47% of 9M20 manufacturing revenue was attributed to previous customers, translating to an estimated c.150% rise in sales generated from these groups of customers. Additionally, we believe there is a level of stickiness in the relationship between MED and its larger customers who may be resistant to seeking alternative PPE producers given the need for quality assessments.

| 2. Post-pandemic strategy – A curated approach. |

MED has been careful not to layout large sums on capital expenditure as the Group is aware of the unsustainable nature of current demand. Most of MED’s output has been met by increasing round-the-clock shift workers, converting idle plants into additional production bases and boosting efficiency.

Going forward, we believe MED will study the viability of establishing new manufacturing bases with a possible focus on Europe. Some countries may turn inward to domestic producers for important medical supplies and MED may expand accordingly to meet these needs.

In addition, MED is looking to further develop its self-branded (CoverU) line of PPE through brand franchising which we think has been well received given the high proportion of 9M20 self-brand sales of 68%.

| 3. Transition away from ODM model to raise ASPs. |

MED’s transition away from an original design manufacturing (ODM) business model is expected to be a key driving factor behind MED’s larger earnings post-COVID. We estimate that ASPs generated from the sales of own branded products could be over double that of sales of non-branded products.

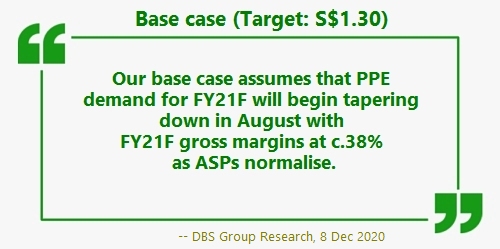

As such, while PPE product ASPs in the market are expected to normalise in future, ASPs recorded by MED’s, while lower than in FY20, are estimated to still remain c.90% higher compared to the preCOVID period.

| 4. Main earnings driver: MED’s future earnings to be sustained by post-pandemic PPE stockpiling. |

Our base case estimates put post-COVID demand for gowns and masks at c.25% and c.5% of demand during pandemic levels, driven by international stockpiling of PPE. We believe that COVID-19 has heightened the awareness and importance of PPE stockpiling and expect most countries that MED serves to stockpile a reasonable 90 days of PPE, creating medium-term demand for gowns and masks after COVID-19.

Notably, MED’s customers are largely from high income nations such as the UK, Germany and the US which we think possess the capability to stockpile. In the longer-term, expiring PPE products may give a permanent boost to PPE demand as governments replenish their stockpiles of PPE.

We observe that PPE shelf lives have a range of between 2 – 5 years and think that countries are likely to spread their replenishment needs evenly over the years.