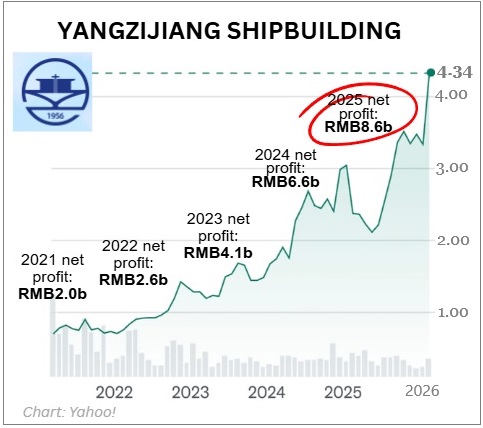

• Feb 2025, a good 12 months ago -- a classic "knee-jerk" reaction by investors happened when the Trump administration proposed port fees on Chinese vessels. Investors dumped Yangzijiang Shipbuilding shares, sending the price tumbling from over $3 to under $2 in just two months.

• Yangzijiang's FY2025 profit growth was intact on top of which the Singapore-listed company declared a high final dividend of S$0.20 (FY2024: $0.12), and analysts reckon this level is sustainable for both 2026 and 2027. • Read excerpts of UOB KH's report below .... |

Excerpts from UOB KH report

Analyst: Adrian Loh

Yangzijiang Shipbuilding

2025: In A Multi-Year Earnings Visibility Phase

| Highlights • YZJ saw record-high shipbuilding margin of 35.1% in 2025, which boosted YZJ’s profitability and earnings quality. • A strong US$22.4b orderbook provides earnings visibility through to 2030, underpinning sustainable dividends and cash flow generation. • Maintain BUY with a higher target price of S$4.60, which implies 17% upside |

Yangzijiang's stock price had been rising with rising profits in recent years, until the US threatened, in Feb 2025, high port fees for Chinese-built ships. The stock has recovered nicely.

Yangzijiang's stock price had been rising with rising profits in recent years, until the US threatened, in Feb 2025, high port fees for Chinese-built ships. The stock has recovered nicely.

| Analysis |

• Handily beating estimates. Yangzijiang Shipbuilding (YZJ) delivered a strong 2025 performance with revenue of Rmb28.5b (+7.4% yoy) generating PATMI of Rmb8.64b (+30.2% yoy) as shipbuilding margins continued to expand on a yoy basis.

|

YANGZIJIANG |

|

|

Share price: |

Target: |

In 2025, YZJ recorded its highest shipbuilding margin since its IPO in 2007 at 35.1%, a yoy expansion of 7.2ppt that was supported by stronger shipbuilding execution, improved operating leverage and favourable contract pricing dynamics, particularly for steel.

• Generous dividends at last. YZJ declared a final DPS of S$0.20, a 67% increase from the S$0.12 from 2024.

Representing a payout ratio of 50%, YZJ stated that this level should be sustainable for both 2026 and 2027, highlighting its confidence in the execution of its orderbook and cash flow generation.

As a result, we have raised our payout ratio to 50% for 2026-27.

• Order wins and 2026 outlook. Despite a difficult 1H25 as a result of Trump’s perplexing policy, YZJ nevertheless managed to secure US$2.5b of new orders, which lifted the outstanding orderbook to US$22.4b.

Importantly, these 245 vessels provide earnings visibility through to 2030.

Management highlighted improving ordering momentum, with global newbuild orders rising 27% yoy in Jan 26, driven by fleet replacement demand.

For 2026, YZJ has pulled back its order win target from US$6.0b to US$4.5b with some remaining slots for 2029 and opening 2030 positions.

• Fine-tuning our earnings. Our earnings estimates for 2026 have seen a mild 1% downgrade while 2027 earnings have been raised by 2% to incorporate a 2-3ppt increase in shipbuilding margins for both years; meanwhile, associate contribution and trading profits have been cut.

● We maintain our BUY rating with a PE-based target price of S$4.60 (previously S$4.10).

We peg the company’s 2027 EPS to a target PE multiple of 10x which is 2SD above the company’s past 10-year average. |

→ Full UOB KH report here.

→ Full UOB KH report here.

→ See also CGS report with a higher target price of S$4.95