Excerpts from OSK-DMG report

|

|

Oxley Tower on Robinson Road is currently 95% sold. Target year of completion: 2017. NextInsight file photo.

Oxley Tower on Robinson Road is currently 95% sold. Target year of completion: 2017. NextInsight file photo.» A phenomenal success story. Oxley was listed three years ago as a boutique developer of residential projects. Post listing, the group diversified across all segments of the real estate market, launching some 28 projects that have since been substantially sold out. The group’s success can be attributed to its dynamic management and strong ability to execute projects.

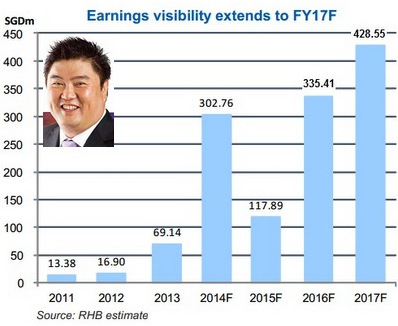

» SGD1.1bn of surplus from Singapore projects. Oxley has chalked up over SGD700m of surplus for its Singapore development projects, which will be recognized over the next 2-3 years. In addition, we expect its first hospitality project, The PINEs, to generate a surplus of SGD380m and a recurring income stream of SGD35m upon completion.

» Overseas projects gaining momentum. Since last year, Oxley has amassed an overseas portfolio of 13 prime sites in Malaysia, the UK, China and Cambodia. It has launched two projects, Royal Wharf in the UK and The Bridge in Cambodia, achieving SGD1bn of pre-sales to be booked over the next 2-3 years. The sustained momentum in upcoming launches could extend earnings visibility into FY18 and beyond.

» SGD1.1bn of surplus from Singapore projects. Oxley has chalked up over SGD700m of surplus for its Singapore development projects, which will be recognized over the next 2-3 years. In addition, we expect its first hospitality project, The PINEs, to generate a surplus of SGD380m and a recurring income stream of SGD35m upon completion.

» Overseas projects gaining momentum. Since last year, Oxley has amassed an overseas portfolio of 13 prime sites in Malaysia, the UK, China and Cambodia. It has launched two projects, Royal Wharf in the UK and The Bridge in Cambodia, achieving SGD1bn of pre-sales to be booked over the next 2-3 years. The sustained momentum in upcoming launches could extend earnings visibility into FY18 and beyond.

Inset: Ching Chiat Kwong, executive chairman of Oxley.» Initiate coverage on the stock with a BUY and a TP of SGD0.91. We value Oxley using a reappraised net asset value (RNAV) method to derive a fair value of SGD3.32bn, or SGD1.14 per share.

Inset: Ching Chiat Kwong, executive chairman of Oxley.» Initiate coverage on the stock with a BUY and a TP of SGD0.91. We value Oxley using a reappraised net asset value (RNAV) method to derive a fair value of SGD3.32bn, or SGD1.14 per share. Our valuation is premised on a summation of Oxley’s current net asset value, and the valuation surplus accruing from its local and overseas projects. We apply a 20% discount to our RNAV to derive a TP of SGD0.91. Initiate coverage with a BUY rating.

» Key risks: While Oxley has executed well on the local front, its track record in overseas markets is limited. Its overseas projects in less developed markets are subjected to greater regulatory and policy risks. Any change in regulations involving taxes on property sales or foreign property ownership could have a direct impact on its sales rate.

Full 48-page report here.

Recent story: OXLEY: Substantial shareholder buys shares following price fall