Excerpts from latest analyst reports...

Analysts: Elaine Khoo, CFA, & Gregory Lui, CFA

The removal of M&A uncertainty should help narrow OUE’s NAV discount,which has hovered at a deep 36% since Oct.

Over the same period,commercial developers have enjoyed tightening of NAV discounts and office REITs are now above book NAV.

OUE offers leveraged exposure to SG commercial with a well-diversified portfolio of prime assets which we favour and limited residential market risk.

Upgrade to Buy with TP of S$3.32 (fr S$2.84) pegged to 25% disc to RNAV.

We have reviewed our estimates with RNAV +2% to S$4.43 and aligned our TP in line with the sector from 35% to 25% with M&A overhang lifted.

As a result we revise up our TP from S$2.84 to S$3.32 (+17%).

Valuations are attractive with the stock at 0.83x P/B and 36% discount to RNAV.

In comparison, valuations for the commercial REITs have tightened significantly and are now at premiums to book.

Downside risks: sharper-than-expected slowdown ingrowth affecting office and hospitality demand, leasing risk for office and acquisition risk.

Related story: 'SUMER': Property prices to fall but some property stocks still undervalued

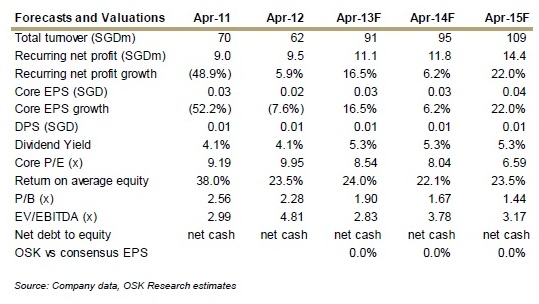

OSK-DMG raises target price of XMH Holdings to 32 cents

Analyst: Lee Yue Jer

Photo by Sim Kih

Two days ago, the Japanese central bank doubled its inflation target and made an open-ended pledge to buy potentially unlimited US government bonds, in effect setting upon a path of quantitative easing.

The structural Yen depreciation will benefit XMH’s business, being dominantly in Yen-denominated Mitsubishi engines.

With XMH having risen 51% and hitting our TP in two months, we review our assumptions resulting in our TP being raised to $0.32. Maintain Buy.

Thank you Bank of Japan! We see the Yen depreciation boosting XMH’s main business over the medium term, which is focused on Indonesian tugboat builders that form about 65%-70% of XMH’s revenue.

Being exclusive distributors of the Mitsubishi brand in multiple countries in this region, the effective price cut will allow XMH a better chance to increase its market share, boosting XMH’s core business outlook.

Recent story: GEO ENERGY, XMH HOLDINGS: Latest happenings

Lim & Tan Securities says Sino Grandness (86 c) is still cheap!

As Sino Grandness is in the midst of preparing for a separate listing of their fruit and vegetable juice business (Garden Fresh) by 2014 (either in Hong Kong or Taiwan), we seek to do a comparative valuation with similar companies listed in Hong Kong/ Taiwan to see how much could it be worth (potentially) if the listing ultimately succeeds.

Consensus is expecting Sino Grandness’ profit to rise 34% in 2013 to Rmb329mln and about 50% of it is derived from Garden Fresh, translating to Rmb165mln.

While much bigger in size than Sino Grandness, comparable companies such as Uni President, Tingyi and Want Want are all trading at an average PE of 25x 2013 earnings.

Assuming we take a 60% discount (10x PE) due to its smaller size, Garden Fresh alone would command a market cap of S$330mln (S$1.24 per share) compared to Sino Grandness’ current market cap of S$228mln (S$0.86).

Sino Grandness’ current market value of S$228mln is only valuing the entire company at 3.5x 2013 earnings.

While its share price has risen a significant 72% since Dec ’12 and is currently at its all time listing high, its continued low 2013 valuation suggests that if the company is successful in listing Garden Fresh in 2014, it remains cheap even at this level.

We maintain BUY.

Recent story: 8 stocks that inspire investor optimism for 2013

Comments

The run up of share price of Sino Grandness, a S-chip, has caught many by surprise.

Many investors have doubts about the brand equity of Garden Fresh for the beverage business is keenly competitive. When signs emerged that Garden Fresh is selling well, and mainly through big supermarket chains, concern turned to the hefty penalty that has to be paid to bondholders if Garden Fresh fails to list in HKSE by Oct 2014.

Judging by the rising sales of Garden Fresh juice, the money from bondholders has been put to good use.

Garden Fresh is selling in more provinces, gradually, and the company plans to reach lower-tier cities in existing provinces. Moreover, the company initially relied on OEMs.

Only after sales had picked up, it decided to have its own juice factory in Sichuan, which is now operating, and another one in Hubei, scheduled to start operations several months from now. In-house production lowers costs and the geographical spread of its own factories and OEMs reduces transportation cost.

Initial concern about failure to list Garden Fresh in HKSE revolved around not being able to fulfil the following profit targets:

2011 RMB 70m

2012 RMB 140m

2013 RMB 250m.

Garden Fresh turned in a profit of RMB 87m in 2011. Indications are that there is no difficulty in crossing the required RMB 140m in 2012, going by the strong performance in the first 9 months of last year.

The penalty that becomes payable if Garden Fresh is not listed in HKSE in time amounts toRMB 560m, against the nominal value of RMB 370m.

With rising profit from Garden Fresh, the company should be in a position to pay this off. The original business of being the OEM of canned vegetables for overseas supermarket chains is doing well as poor economies in Europe drive many to shop for cheaper foods from China.

Being the OEM that cans vegetables under the labels of big overseas supermarket chains also provide Chinese consumers food safety assurance as Sino Grandness expands sales of non-beverage products domestically.

he nascent canned fruit business seems to has prosper, earning high margins.

It may sound odd that failure to list in HKSE may not be bad after all. A successful listing will result in the bondholders having a 25% stake in Garden Fresh valued at six times of RMB250m. It will not be unrealistic to expect a higher price earnings ratio of 15 times. Moreover, the likelihood of Garden Fresh exceeding RMB 250m in 2013 is not far-fetched, and the juice company should have a much higher valuation.