Excerpts from Standard Chartered Equity Research's 120-page report published this morning on the Singapore healthcare sector

Analysts: Stephen Hui, Magnus Gunn, Pauline Lee

The investment case for healthcare in Singapore is exceptionally robust, in our opinion. In this note, we provide an analysis of the growth drivers for healthcare spending that goes beyond traditional demographics. Based on our conclusions from this analysis, we have a high degree of confidence in the ability of certain business models to sustain future earnings growth, which should translate into continued long-term alpha for appropriately positioned investors.

Our analysis shows the overall market for private tertiary healthcare spending in Singapore growing at a 7% CAGR until 2020E: The drivers are: (1) population growth of 2%, (2) impact from an aging population of 1.4% and (3) a shift towards private healthcare at 0.4%. We anticipate the biggest driver will come from a fourth factor: demand for ever more specialist services and care (‘revenue intensity per patient’), which we expect to persist at 3% until 2020.

Our 7% estimate for tertiary healthcare spending refers to the overall market and we estimate that certain players, such as Raffles, will sustain far higher growth rates.

We believe direct competition will remain limited due to strong market segmentation, especially for two of the three private hospital operators: Raffles Medical (Raffles), which is the leader in the corporate segment and Thomson Medical (Thomson), which specialises in women and children. For Parkway Holdings (Parkway), the dominant provider in the high-end patient market, we believe the completion of the Farrer Park Hospital in 2012/2013 will signal increased competition ahead, although we do not anticipate a significant impact.

We expect the growth in the foreign patient market will return as the global economy recovers, providing an additional growth driver. The key read across from our visits to three listed ASEAN hospital operators is that there is limited direct competition with Singapore as they largely target different source countries. For the Indonesian market, Singapore has a durable competitive advantage due to proximity and established relationships.

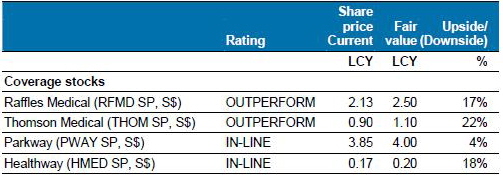

Recommendations: We have OUTPERFORM ratings on Raffles and Thomson and IN-LINE ratings on Parkway and Healthway. In our view, Raffles has the most robust and defensive business model and has operating leverage through expansion of its specialist services. We like Thomson’s specialty leadership in birth deliveries and its attractive valuations. We downgrade Parkway from OUTPERFORM to IN-LINE to reflect the stock’s current high valuations. Healthway is expanding aggressively and has strong potential, in our view, but given recent staffing issues we will await further execution before taking a more positive view.

Our approach to valuation is twofold. First, we use a DCF to capture what, in our opinion, is a fairly predictable stream of long-term cash flows. We recognize, however, that the stock market will not build in the full value potential of these businesses (though an industry buyer often will) and investors will still rely heavily on short-term earnings multiples in setting the price. Second, we set our 12-month fair value with reference to peak earnings multiples from the prior cycle, given our bullish views on these companies and in the belief that their long-term earnings potential is becoming better understood by the market.

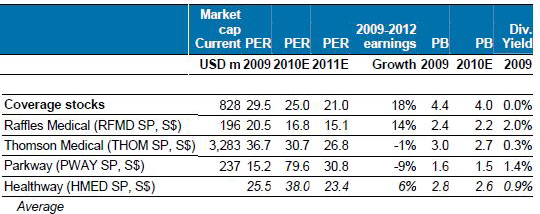

* Our fair value of S$2.5 for Raffles offers potential upside of 17%. The stock is trading on 21x 2011E and our fair value is based on a PER target multiple of 25x 2011E. Raffles’ previous peak valuation was in January 2008 at a forward PER of 25x. Our DCF valuation results in a fair value closer to S$2.8. We like Raffles for its robust and defensive business model and its operating leverage through the expansion of its specialist services. In 2009, Raffles’ hospital business (hospital and specialist services) posted an operating margin of 26% compared with 8% for its primary services. As the group continues to expand its specialist services, we expect continued margin expansion.

* Our fair value of S$1.1 for Thomson offers potential upside of 24%. Thomson is currently trading on PER 15x 2011E and our fair is based on a target multiple of PER 19x 2011E. Thomson’s previous peak valuation was in June 2007 at PER 20x 12-month forward earnings. We like Thomson’s leadership in birth deliveries and its long-established brand name.

Thomson hospital is running at near full occupancy and this may present concerns on its future growth profile. But, our analysis shows that Thomson should still have room to grow.Together with its attractive valuations, we believe there is significant upside to its share price.

* Our IN-LINE rating for Parkway is based on valuations. Our fair value of S$4 translates to PER target multiple of 29x 2011E. The stock is currently trading on 27x PER 2011E on our core earnings estimate which strips out the gain from sales of the company’s Novena medicalsuites. In July 2007, the stock had traded at PER 40x 12-month forward earnings. Our target multiple is at a discount to peak valuations as our DCF shows fair value of S$4.34, offering only 13% upside (in contrast, Raffles’ DCF fair value offers over 30% potential upside). In our view, Parkway is the pre-eminent healthcare franchise in Asia due to its dominant position in Singapore and wide geographical reach. We believe the upcoming Parkway Novena hospital will strengthen the group’s position in its home market but uncertainties remain as to the hospital’s operating performance.

* Our IN-LINE rating for Healthway stems from our “wait and see” approach. We believe Healthway has tremendous potential through its aggressive expansion of its services in Singapore and China. But in 1H 2010, its profit fell by 82% and management has advised this was due to the departure of key specialists and the costs associated with new clinics. In our view, the situation for Healthway is rather binary. If its new clinics succeed in building up a customer base, the share price would have significant upside.

If it does not execute, its share price has significant downside potential as the stock is now trading at PER of 30x 2011E, which we believe already factors in a sharp bounce in profit.