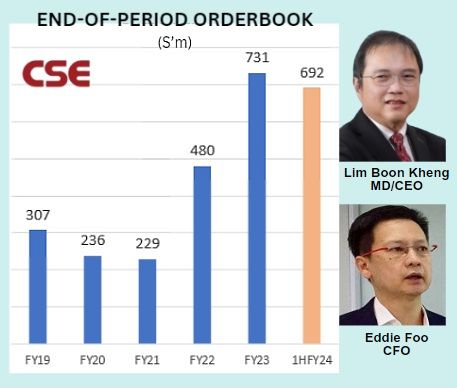

• Investor sentiment towards CSE Global ran high on Sept 9 (Monday) after an analyst report shared on-the-ground insights into the company's "electrification" segment potential in the US. Within the same day, sentiment took a nose dive after CSE, during market off-hours, said it had to settle a legal claim for US$8 million. Ouch! You can imagine the shock waves that hit.  The stock plummeted from 47 cents to as low as 41 cents the next day. The stock plummeted from 47 cents to as low as 41 cents the next day.• The analyst, from Maybank Kim Eng, had a quick follow-up report, lowering his target price and earnings forecast -- but reiterated his conviction on the mid-term prospects of the "electrification" business potential in the US. The stock currently seems to have recovered slightly to 43 cents. • As background, CSE's "electrification" segment is engaged in projects that enhance electrical infrastructure, which includes working on substations, switchgear, switchboards, and transformers. These projects are crucial for upgrading power systems to meet increasing demand. • That segment has contributed to a strong orderbook for the group. See the chart below.  Electrification segment accounted for S$395 m of the 1HFY24 outstanding orderbook. The other segments: Automation (S$191 m), Communication (S$106 m). Electrification segment accounted for S$395 m of the 1HFY24 outstanding orderbook. The other segments: Automation (S$191 m), Communication (S$106 m).• CSE counts Temasek Holdings as its No.1 shareholder (~23% stake) and the Singapore Government as one of its clients. Read excerpts of Maybank's latest report below .... |

Excerpts from Maybank KE report

Analyst: Jarick Seet

A bump in the road

We view this as a one-off road bump and remain positive on CSE’s prospects. However, we reckon that management should do a post mortem and come up with better systems and procedures to ensure smoother project execution after the settlement. We also factor in the settlement charge and lower our FY24/25E PATMI by 27.2% and 17.3%, respectively, and cut our TP to SGD0.60 from 0.64 with a lower P/E multiple of 13x from 15x to factor in higher execution risk for its projects. Maintain BUY. |

| Delay in performance of contracted works |

Hankin was engaged by the claimant to perform certain engineering, materials procurement and installation services on a construction project in the US for which the Claimant was the general contractor.

|

CSE |

|

|

Share price: |

Target: |

It alleged that it suffered losses due to Hankin’s delay in its contracted works.

To its defence, Hankin has alleged that the delay stemmed from Covid-19 supply chains disruptions and late variations in the client’s instructions.

The claimant issued arbitration proceedings in the US on 3 Sep 2024 and on 8 Sep 2024, a full and final settlement of all claims for USD8m was reached, subject to the execution of a written settlement agreement and release by the parties.

This payment will be reflected in CSE’s FY24E numbers.

| Internal processes need improvement |

Jarick Seet, analystAfter this settlement, management will need to improve its internal processes and systems or its contract terms to prevent and mitigate such incidents from happening again, despite it being a key risk of this business.

Jarick Seet, analystAfter this settlement, management will need to improve its internal processes and systems or its contract terms to prevent and mitigate such incidents from happening again, despite it being a key risk of this business.

We will be keeping an eye on this and also execution of its other projects.

| Mid-term outlook still positive and intact |

We believe that this is a hiccup for CSE and it will have to improve its execution efficiency and learn from this incident.

We remain bullish on the electrification landscape and opportunities and management’s capability to steer the ship back to the right path again.

We also expect further contract wins in the electrification space in the near term ranging from SGD50-100m as well as potential share-buy backs to show confidence.

See full report here.