|

XMH acquired Mech-Power last year from Mrs Corrine Loke, controlling shareholder of Mech-Power (extreme right) and her husband, Clive (extreme left). With them is Elvin Tan, chairman of XMH. Photo: Company XMH acquired Mech-Power last year from Mrs Corrine Loke, controlling shareholder of Mech-Power (extreme right) and her husband, Clive (extreme left). With them is Elvin Tan, chairman of XMH. Photo: Company

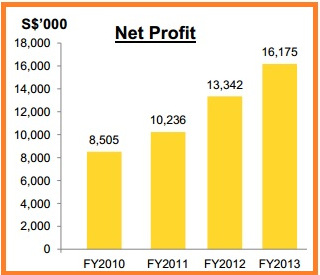

Mid-term growth outlook intact. We continue to like XMH for its clear mid-term growth potential from: |

OSK-DMG says Enterprise of the Year award for Mencast reflects its growth potential

Analyst: Lee Yue Jer

Glenndle Sim, executive chairman of Mencast. NextInsight file photoMencast received the Enterprise of the Year award at yesterday evening’s Singapore Business Awards presentation dinner. Other preeminent companies that have won this award include Tee Yih Jia Food Manufacturing, Super and The Coffee Bean & Tea Leaf.

Glenndle Sim, executive chairman of Mencast. NextInsight file photoMencast received the Enterprise of the Year award at yesterday evening’s Singapore Business Awards presentation dinner. Other preeminent companies that have won this award include Tee Yih Jia Food Manufacturing, Super and The Coffee Bean & Tea Leaf. The win reinforces our view of Mencast as a long-term growth player in the oil & gas (O&G) industry. We maintain our BUY call and SGD0.76 TP.

Excellence in all criteria. The Enterprise of the Year Award recognises companies along four criteria: i) innovation record, ii) entrepreneurial skills, iii) growth record, and iv) financial performance.

Mencast has indeed successfully reinvented itself to encompass multiple points in the maintenance, repair and overhaul (MRO) business along the O&G value chain from just a sterngear manufacturer initially.

History as a guide. Tee Yih Jia Food Manufacturing Pte Ltd, whose executive chairman Sam Goi won the Businessman of the Year Award last night, was the first Enterprise of the Year Award winner in 1986.

Recent winners include Super (SUPER SP; BUY; TP: SGD3.99) in 2012, The Coffee Bean & Tea Leaf in 2011 and YCH Group Pte Ltd in 2010.

If history is any guide, we hope to see Mencast achieving the same prominence in the O&G industry as these others have in theirs.

If history is any guide, we hope to see Mencast achieving the same prominence in the O&G industry as these others have in theirs. Sending a strong positive signal to all stakeholders. We believe that this award sends a strong signal to all stakeholders on Mencast’s sustainability and growth potential.

We continue to see clear sources of growth in each of its offshore and Engineering, Marine, and Energy divisions, notwithstanding the labour supply issues in Singapore. Its heavy investment in automation and productivity improvements should begin to bear fruit this year.

Maintain BUY with SGD0.76 TP unchanged. This award serves to reinforce our view of Mencast as a long-term growth player in the O&G industry. Our TP is based on 12x recurring FY14F P/E, which is a conservative multiple for its 80% core earnings growth potential this year.

Recent story: YANGZIJIANG, MENCAST: What analysts now say