OLAM INTERNATIONAL, a leading global, integrated supply chain manager and processor of agricultural products and food ingredients, has reported Profit After Tax and Minority Interest (PATMI) of S$370.9 million for FY2012.

This is 13.7% lower compared to S$429.8 million in FY2011.

PATMI excluding exceptional items declined by 4.6%.

The board recommended a final dividend of 4.0 cents per share.

For details of the FY12 results, click here.

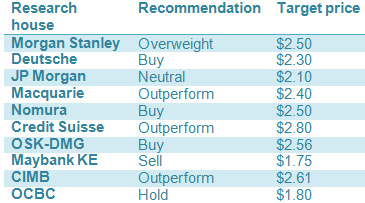

Excerpts from latest analyst reports on Olam International.....

Compiled by NextInsight

> Morgan Stanley: We remain OW, as we find the valuation attractive and the food business solid.

The outlook for F2013 is better, driven by solid growth in foods with key initiatives scaling up well and normalization in non-food.

The stock is trading at 13.3x NTM P/E, which is a 20% discount to its two-year average P/E and on C2013e EPS, Olam trades at a 15% discount to its relative SOTP multiple.

> Deutsche Bank: We increase our beta assumption from 1.3 to 1.4, in line with the increase in volatility of the stock.

As such, our target price falls from S$2.90 to S$2.30 (COE 10.5%, WACC 7.8%, terminal growth 4%), implying 11x CY13E EPS.

Olam has so far bought back 52.2m shares (2.14% of total shares) since the launch of its first-ever share buyback program on 8 June.

Key risks include political instability in countries of operation, integration risk for new businesses acquired.

> JP Morgan: Key takeaways from analyst briefing:

(1) Management reiterated its 2016 net profit target of US$1 billion with RoE of >25% with no incremental equity raising although its FCF positive year now targeted by 2015,

(2) Mid-teens RoE targeted over next 12-18 months,

(3) food segment largely strong across (except tomatoes),

(4) Significant increase in overhead costs as it has entered new businesses and expects related costs to see slower growth moving forward,

(5) Seen tax reversal in 4Q12 on lower tax in OECD markets.

> Macquarie: Maintain Outperform. While expecting shares to be weak following results, based on our proprietary asset by asset build up analysis, we see Olam’s medium term story as compelling.

Our target price implies 12.3x FY13E PE on the stock, giving 21% price upside.

However, investors will have to be patient. Meanwhile we continue to prefer the upstream CPO names, GGR and FR than midstream plays.

> Nomura: With Olam’s stock having done well recently (up 20% in the last three months), and no visible near-term catalyst (1Q for Olam is a non-event, and the Gabon financial closure is a few months away), we expect some near-term weakness in the stock.

We still like Olam’s long-term story and fundamental asset shift to upstream/midstream, and believe it will take some time for assets to fully ramp up.

> Credit Suisse: Lower our forecasts on lower food staples/packaged foods segment NC/ton contribution.

Valuations remain undemanding at 12x FY12E P/E, given 24% EPS CAGR; its share buy-back programme lends support.

Maintain OUTPERFORM; cut TP to S$2.80.

>OSK-DMG: We lowered our FY13 net profit forecast by 6% to factor in continued cotton and wood weakness and higher costs.

Remain positive on food, which accounted for 87% share of net contribution.

Olam trades at a FY13F P/E of 10.8x, which is inexpensive versus FY13F net profit growth of 21%.

Maintain BUY with an unchanged target price of S$2.56, derived from a 3-stage DCF valuation model. Our TP translates to a FY13 P/E of 13.9x, which is lower than the historical average of 17x.

> Maybank KE: Maintain SELL. We think earnings headwind could continue for at least 1-2 more quarters, especially from the IRM segment.

We maintain SELL, with a TP of SGD1.75, pegged to 1.2x P/B, given the lack of earnings visibility at the moment.

> CIMB: Olam’s 4Q12 core net profit missed expectations as profits were eroded by high opex incurred for business expansion, while industrial raw materials remained a drag.

Nevertheless, we sense that the worst is over and the group will reap rewards as acquisitions start to pay off.

> OCBC: In light of the still muted outlook, we pare our estimates for FY13 revenue by 9.8% and core earnings by 6.0%.

Hence even as we roll forward our unchanged 12.5x peg to FY13F EPS (from blended FY12/FY13 previously), our fair value drops to S$1.80.

Maintain HOLD and would only consider accumulating around S$1.60 or better.

Recent story: OLAM triple buying of shares; SAMKO shareholder continues buying

Comments

Effectively, EPS has declined by about 30%. At current share price, its normalised PE is around 19x which is on a high side. At 13x PE, its share value should be around 1.30, so there should be more downside pressure on its share price.

Now I look at its gearing. Total debt stood at $7.489 billion while its equity stood at $3.528 billion. It gross debt gearing is a huge 212%. Even if I net its cash of $1.1 billion off its total debt, its net gearing is a huge 181%. Worse still, its current debt maturity stood at $3.148 billion.

I wonder how Olam is going to discharge its debt obligation.. and what happen if its biological assets value start to decline? 4 cents dividend translate to a mere 2% dividend yield. My advice to long-term investors is to avoid this counter, no matter how good those analysts talk about its upside and potential.