HONG KONG-listed China Qinfa Group Ltd (HK: 866) was apparently a bit modest in its late July positive profit alert in which it alerted investors that the Jnuary-June bottom line would likey jump around 1,000% year-on-year.

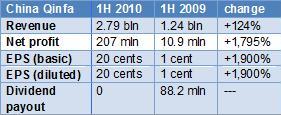

In fact, the coal purchaser, processer, trader and deliverer just announced that its first half net profit rose to nearly 206 mln yuan, up 1,796%!

Turnover in the first six months was 2.79 bln yuan, up 123.8% from a year earlier.

A quick look at the company’s revenue stream for the period reveals the core reasons for their very successful half.

Coal trading volume over the period rose 213.4% year-on-year to nearly five mln tons.

Shareholders were the biggest beneficiaries, as basic earnings per share in the first half skyrocketed some 1,900% from a year earlier to 20 cents (RMB).

However, Qinfa’s Board of Directors also announced that shareholders would have to be happy with their earnings as it recommended no interim dividend payment compared with an 88.2 mln yuan payout a year earlier -- most likely a clear signal that the company would continue to expand its fleet and facilities when strategically advantageous.

Qinfa remains principally engaged in the coal operation business involving purchase and sales, filtering, storage, blending, shipping and transportation of the commodity which along with oil is sometimes nicknamed "black gold."

“Since the beginning of the fourth quarter in 2009, the global economy has gradually recovered from the financial crisis. There has been a revival in market demand for thermal coal for electricity generation.

"The increase in demand continued during the first half of 2010. Hence, we achieved significant growth in the trading volume of coal as compared to the same period in 2009,” said China Qinfa Chairman Xu Jihua.

And the sustained demand recovery naturally translated in higher selling prices, which in the first half ranged on average between 538-602 yuan per per tonne – “significantly higher” than the 400-489 yuan a year earlier, Qinfa added.

“Taking advantage Qinfa’s extensive procurement network and international trade experience, we sourced coal from various overseas suppliers. The volume of coal imported by Qinfa to China amounted to approximately 69.1% (compared to 74.8% a year earlier) of our total coal purchases in the first half,” Chairman Xu said.

China Driving Outlook

Although the global economy has recovered from the financial crisis and international commodity markets are generally stabilized, China Qinfa still believes there are still lingering uncertainties including unresolved EU debt crises, the potential for tightened liquidity and policy shifts in China.

“These could adversely affect demand for electricity in China and demand for thermal coal in the second half of 2010. However, we will continue to take advantage of the continuous economic growth in China,” Chairman Xu said.

He added that the level of domestic production and consumption in China will likely continue to increase steadily.

“These will stimulate demand for electricity, with thermal coal as the principal raw material for power generation.”

Due to the anticipated increase in the demand for coal products, Qinfa said it will continue to improve its business model with the following activities:

A joint venture agreement was established in October 2009 with Hebei Port Group to construct and operate the Zhuhai Terminal. The JV will will be 60% owned by Qinfa which will contribute a total of 311.4 mln yuan.

The JV is strategically located in the southern province of Guangdong, thus allowing Qinfa to take advantage of its proximity to customers located in the coal consuming coastal cities of South China, react more quickly to customers’ needs, and lower transportation costs.

The berthing capacity of Zhuhai Terminal is 100,000 DWT which enables it to accommodate Capesize and Panamax vessels for coal transshipment.

“We will be able to further strengthen our coal storage and blending capacities as Zhuhai Terminal can serve as a site for both activities. And as it will have an annual throughput capacity of 20 mln tonnes which can also serve as a centre for coal exchange, it can advance our ability to further procure and trade coal,” the chairman added.

Zhuhai Terminal is expected to commence operation in the second quarter of 2012.

Qinfa placed confirmed orders for the construction of two additional 82,000 DWT bulk carriers in May 2010 at a total cost of 538.2 mln hkd.

“We have been planning to improve the efficiency of our fleet and the construction of vessels is consistent with this plan. Also, as our coal trading volume continues to expand, the increase in the number of our own vessels -- and thus shipping transportation capacity – could enhance our control over trading costs and reduce exposure to transportation cost fluctuations,” Chairman Xu said.

Qinfa is also actively looking for opportunities to expand its customer base, developing business relationships with new sizable domestic power groups in China.

“The expansion of our customer base is an important strategic step and will help us develop coal production and sales and expand our income sources,” he added.

In addition, Qinfa is actively looking for suitable locations in Inner Mongolia for the construction or acquisition of additional coal loading stations, and also acquisition opportunities of existing coal stations along the Daqin Railway in Northeast China in order to strengthen its coal processing and transportation capacity in the region.

Vertical Integration

Qinfa considers acquisition of coal mines or equity interests in coal mining companies crucial in reinforcing the company’s vertically integrated supply chain of coal.

“This vertical integration strategy will enable us to secure a stable supply of coal, both in terms of quality and quantity, for our customers which then can enhance our competitiveness as well as strengthen customer ties. Therefore, we will continue to identify domestic and overseas coal-related development projects for acquisition or business cooperation in order to further integrate our coal supply chain,” the chairman said.

In order to secure a stable coal supply amid fluctuating prices, China Qinfa took full advantage of opportunities arising from substantially lower coal prices last year by signing an equity transfer deal in August 2009 to acquire an 87.88% equity stake in Ruifeng Coal for a consideration of 130 mln yuan, with the deal completed in February this year.

Ruifeng Coal in northern China’s Shanxi province is the owner and operator of a coal mine near the city of Datong, with the mine having approved annual production capacity of 900,000 tonnes.

“The mine shaft has a coal reserve of over 59 mln tonnes and the coal is of prime thermal grading. Located 70 kilometers from Qinfa’s existing coal loading station in Datong, the mine enjoys convenient transportation links. Our directors expect that the coal mine will commence pilot production in the second half of this year,” Chairman Xu said.

See also: CHINA QINFA: Expects Tenfold 1H Net Profit Spike