Excerpts from analysts' reports

Maybank Kim Eng estimates Valuetronics' fair value is 61 cents

Maybank Kim Eng estimates Valuetronics' fair value is 61 cents

|

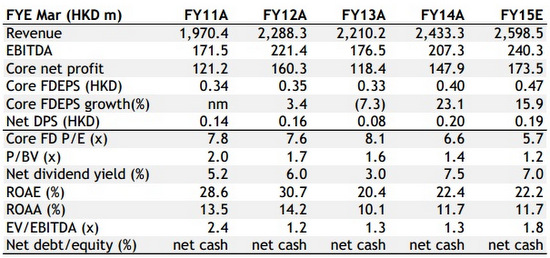

§ Company continues to trade at an undemanding valuation of 5.7x FY15E P/E (and only 2.9x on ex-cash basis) vs. the peer average of 8.3x. FY15E yield forecast to be 7%. |

Valuetronics has indicated that the LED business stems from one large multinational customer but it does not disclose the product/client contribution breakdown. Maybank KE has assumed that most of the LED business is driven by Philips – the global leader for LED, lightings & luminaries.

Valuetronics has indicated that the LED business stems from one large multinational customer but it does not disclose the product/client contribution breakdown. Maybank KE has assumed that most of the LED business is driven by Philips – the global leader for LED, lightings & luminaries.

Refocusing on the core

After 3 years of trying to turnaround the licensing business, Valuetronics made a decisive move to exit the business in FY13 and refocus on its core OEM/ODM business in Consumer (CE) and Industrial & Commercial (ICE) Electronics. Strong demand for LED luminaries worldwide will be the dominant catalyst for CE business (68% of total revenue) - most of the business is driven by a single major customer, who also happens to be the global leader for LEDs lights.

On the ICE front, renewed efforts to grow customer base and wallet share should reinvigorate the sales mix and improve margin outlook.

A cash generative business that is under-appreciated

Valuetronics has consistently delivered ROEs in excess of 20% over the last 4 years and maintained free cash positive for 9 of the last 10 years.

The company has zero debt and S$0.21/share of cash (close to half of its share price).

Stock trades at 5.7x FY15E PE but stripping out cash, valuation falls to only 2.9x FY15E PE. Assuming a conservative 8x FY15E P/E, we estimate Valuetronics to be worth S$0.61/share, an implicit 43% upside.

We also believe management can commit to its dividend policy of 30%-50% payout given their solid track record. Our forecast yield is 7% for FY15E.

Recent story: VALUETRONICS: "Cash-rich, 8.1% dividend yield, too cheap to ignore"

Valuetronics has consistently delivered ROEs in excess of 20% over the last 4 years and maintained free cash positive for 9 of the last 10 years.

The company has zero debt and S$0.21/share of cash (close to half of its share price).

Stock trades at 5.7x FY15E PE but stripping out cash, valuation falls to only 2.9x FY15E PE. Assuming a conservative 8x FY15E P/E, we estimate Valuetronics to be worth S$0.61/share, an implicit 43% upside.

We also believe management can commit to its dividend policy of 30%-50% payout given their solid track record. Our forecast yield is 7% for FY15E.

Recent story: VALUETRONICS: "Cash-rich, 8.1% dividend yield, too cheap to ignore"