|

Valuetronics’ FY26 results and, to a large extent, its new capital management plan have triggered a run-up in the stock price. Both UOB KH and PhillipCapital note the changing composition of Valuetronics' revenue. |

Financial Projections: A Consensus on the Next Two Years

Despite slightly different models, both brokerages are quite aligned on Valuetronics’ projected revenue and net profit for the next two years.

Here is the tabulated comparison of their projected revenue and net profit:

|

Brokerage |

FY27F Revenue |

FY27F Net Profit |

FY28F Revenue |

FY28F Net Profit |

|

Phillip Capital |

HK$1,719 m |

HK$163 m |

HK$1,825 m |

HK$171.7 m |

|

UOB KH |

HK$1,668 m |

HK$160 m |

HK$1,714 m |

HK$174 m |

Where They Differ: Valuation and Target Prices

A striking divergence between the two reports lies in their target prices and valuation methodologies.

PhillipCapital raised its target price from S$0.96 to S$1.29.

Analyst Paul Chew relied on a straightforward valuation model, applying a 20x PE multiple to FY27e earnings to reflect an industry re-rating.

|

Brokerage |

Previous Target Price |

New Target Price |

|

PhillipCapital |

S$0.96 |

S$1.29 |

|

UOB Kay Hian |

S$1.03 |

S$1.88 |

However, Chew maintains a cautious tone: "We expect sluggish earnings in FY27e... The jump in effective tax in Hong Kong and Vietnam will be another drag on FY27e earnings".

He also cites: "An increase in component costs and lead times, such as for memory and CPU, will be another challenge for gross margins."

| Attractive value |

"VALUE is currently trading at only 10x FY28F ex-cash PE and offers an "VALUE is currently trading at only 10x FY28F ex-cash PE and offers anattractive FY28 dividend yield of about 6%. We believe valuations remain undemanding, given VALUE’s defensive earnings profile and strong cash generation." -- John Cheong (photo) & Heidi Mo, UOB KH |

Conversely, UOB Kay Hian aggressively raised its target price by 83%, from S$1.03 to S$1.88.

Analysts John Cheong and Heidi Mo arrived at this significantly higher valuation by utilizing a 19x ex-cash PE multiple rolled forward to FY28.

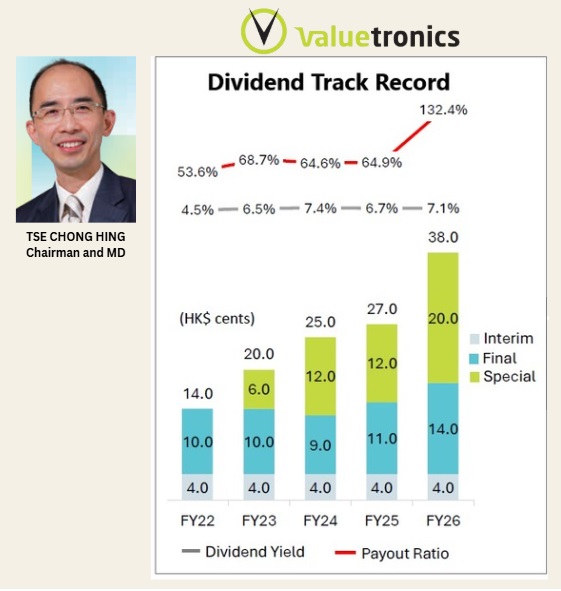

Because Valuetronics holds a massive net cash pile of over HK$1.2 billion—roughly 42% to 50% of its market capitalization—stripping this cash out of the valuation makes the underlying business look much cheaper.

John and Heidi highlight this hidden value: "VALUE is currently trading at only 10x FY28F ex-cash PE and offers an attractive FY28 dividend yield of about 6%. We believe valuations remain undemanding, given VALUE’s defensive earnings profile and strong cash generation".

While both PhillipCapital and UOB Kay Hian foresee similar modest growth and applaud the HK$300 million capital return plan, your view on Valuetronics ultimately depends on your valuation philosophy. |

→ See also:VALUETRONICS: Stock +16% As Investors Cheer New Dividend Policy, HK$300M Cash Return

→ See also:VALUETRONICS: Stock +16% As Investors Cheer New Dividend Policy, HK$300M Cash Return