|

For years, investing in coal stocks was perhaps a relatively simple bet: if coal price went up, the miners made more money, and vice-versa. |

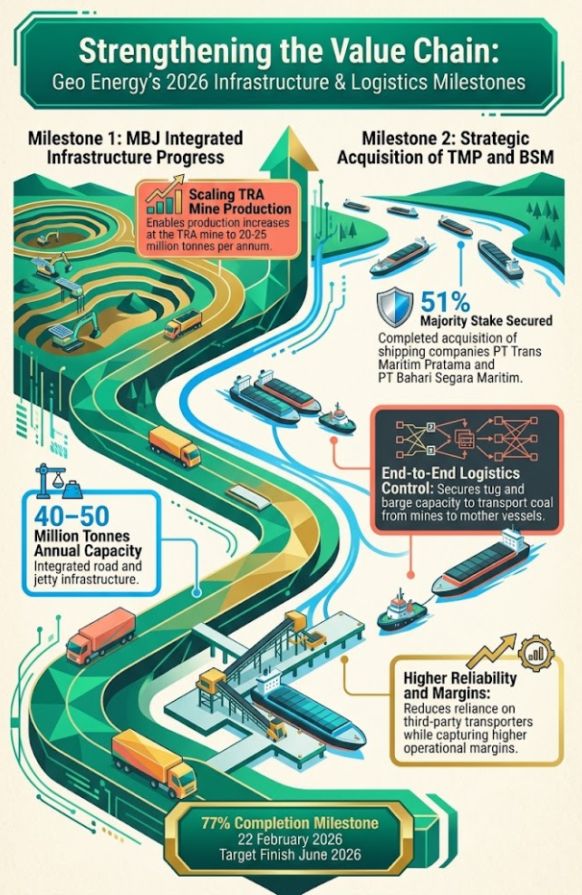

Geo Energy is transitioning from a price-taker to a steady-state infrastructure powerhouse. Here is the investment thesis for Geo Energy.

The Problem: The "Logistics Bottleneck"

While Geo Energy owns the massive TRA mine, getting that coal to market has been expensive and slow.

They’ve relied on small trucks using public roads—a process that is weather-dependent, high-cost, and limits how much they can actually sell.

The Solution: The 92km "Game Changer"

The core of the investment thesis today isn't the coal itself; it’s a 92km dedicated hauling road and jetty (the MBJ project).

As of March 2026, this project is roughly 80% complete with potential benefits illustrated here:

When this road opens in mid-2026, it transforms the business in two massive ways:

-

Drastic Cost Savings: Moving coal via a dedicated private road saves an estimated US$10 per tonne, a massive margin expansion.

-

Volume Explosion: With the bottleneck removed, Geo Energy can scale production from roughly 2–3 million tonnes at the TRA mine toward a goal of 20–25 million tonnes.

The New Business: Becoming a Toll Collector

Perhaps the most exciting part of the thesis identified by Phillip Securities' Paul Chew and KGI's Alyssa Tee is that Geo Energy is becoming a "landlord."

The company is renting it out to neighboring mines, and has already secured 9 million tonnes of third-party "tolling" commitments.

This is recurring, high-margin income that doesn't fluctuate as much as coal prices.

At full capacity, this infrastructure could generate EBITDA levels of up to US$300 million annually which dwarf the company’s traditional mining profits.

The Numbers: What are Analysts Saying?

Analysts are increasingly bullish, though they differ on the target prices for the stock:

-

KGI Securities is the most optimistic, setting a target price of S$1.02, citing the recent surge in coal prices and a low risk of project failure now that construction is nearly finished.

-

Phillip Securities recently upgraded its view to a S$0.75 target, and is more conservative on coal prices but sees the "trifecta win" of higher volumes, better margins, and new fee income.

Forecasts for FY26 and Valuation Comparison

|

Metric (FY26F) |

KGI |

Phillip |

Variance Notes |

|

Revenue (US$m) |

650.6 |

573.0 |

|

|

PATMI (US$m) |

71.5 |

56.8 |

Differing tax rate assumptions (25% vs 30%). |

|

DPS (SG Cents) |

1.9 |

1.3 |

KGI assumes higher payout on infrastructure scaling. |

|

Target price (SGD) |

$1.02 |

$0.75 |

The S$0.27 gap in target prices is primarily driven by:

- Risk Discounting: Phillip lowered its infrastructure valuation discount to 50%, whereas KGI appears to have aggressively removed most execution risk given the 80% completion milestone.

- Discount Rates: KGI uses a 7.93% WACC versus Phillip’s 12%, a significant driver for the S$1.02 target.

2025 saw the lowest ASP and the lowest cash profit/tonne --- all of which are set to reverse sharply in 2026.

|

Year |

Sales volume (Mt) |

ASP (US$/t) |

Prodn volume (Mt) |

Prodn cash cost (US$/t) |

Cash profit (US$/t) |

|

2021 |

11.4 |

56.42 |

10.9 |

31.37 |

25.05 |

|

2022 |

10.2 |

72.14 |

10.3 |

43.10 |

29.04 |

|

2023 |

8.4 |

57.88 |

8.6 |

45.69 |

12.19 |

|

2024 |

7.9 |

50.69 |

7.8 |

40.32 |

10.37 |

|

2025 |

12.8 |

44.12 |

12.5 |

34.10 |

10.02 |

2025 was a rocky year for dividends due to a spike in Indonesian taxes.

However, the outlook for 2026 is much brighter. |