|

Primary-listed on SGX in August 2025 and, more recently delisted from the Hong Kong Stock Exchange, PC Partner saw its revenue and profit surge in 2025.

|

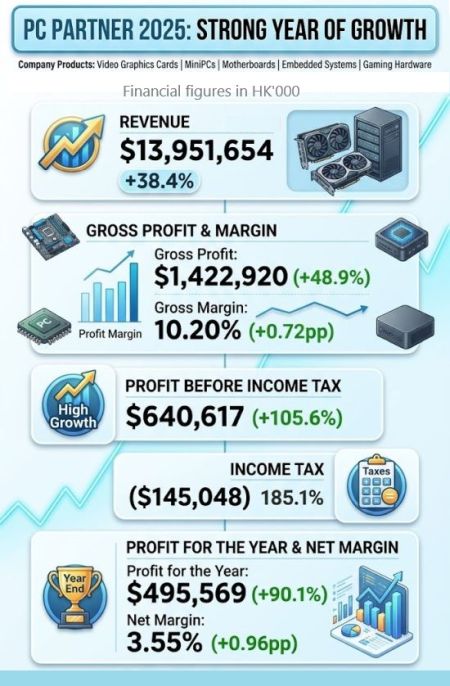

Several key metrics of its FY2025 performance:

A massive boost to its 2025 performance came from the RTX 5090—a product line unavailable to PC Partner in 2024—which contributed HK$1.7 billion, representing 16% of total brand graphics card revenue.

Furthermore, on higher bank borrowings, the company strategically managed its supply chain by aggressively taking in more GPUs in November and December 2025.

This expanded inventory from HK$843 million to HK$1.7 billion (as at end-2025) to avert future shortages.

The company also navigated significant one-off tax expenses, including a HK$63.4 million charge related to offshore manufacturing claims (see table above).

PC Partner proposed a final dividend of 5 Singapore cents and a special dividend of the same amount.

|

Year |

Total Dividend (HK$) |

Dividend payout ratio |

|

2025 |

0.850* |

66.9% |

|

2024 |

0.350 |

51.5% |

|

2023 |

0.300 |

187.5% |

|

2022 |

1.050 |

58.0% |

|

2021 |

2.450 |

39.9% |

|

*5 SG cent final dividend + 5 SG cent special dividend |

||

Challenging New Business Landscape

CFO Gary Lau outlined several headwinds reshaping the 2026 business landscape.

The desktop gaming market is becoming increasingly challenging due to skyrocketing component costs.

Prices for system memory have more than tripled, solid-state drive (SSD) costs have doubled, and both CPU and graphics memory prices are steadily climbing.

He estimated that building a gaming PC is now 30% to 40% more expensive, which threatens to discourage consumers from upgrading their systems or buying new graphics cards.

Compounding the pricing issue is an imminent supply constraint.

As semiconductor resources are heavily reallocated to AI chip production, GPU allocations for the gaming sector from Nvidia will to drop in 2026, with estimates pointing to at least a 20% decline.

With no new consumer GPU generation expected from Nvidia in 2026, the market will rely on existing Blackwell chips.

PC Partner’s Strategy: Premiumization and AI Expansion

To navigate these market shortages and rising costs, PC Partner is adopting a business strategy focused on premiumization.

| "The [ASP] of our own brand graphic card will increase and should drive a higher GPM that can likely offset the volume decline impact." --CFO Gary Lau |

Because low-end GPUs are being discontinued by Nvidia and its partners, PC Partner will aggressively upsell premium products to capture higher profit margins.

Prices have already been increased to compensate for rising memory costs and reduced GPU allocations.

Despite forecasting lower unit volumes, management is confident that price hikes and improved margins will drive revenue growth of 10% to 15% in 2026.

Beyond traditional gaming hardware, PC Partner is actively pivoting toward the enterprise AI boom.

To support this, PC Partner is launching a new R&D center in Taiwan to recruit AI engineers and build out its engineering capabilities. While the company will attend Nvidia's GTC event in March 2026 and actively engage potential customers, Gary cautions that the new AI server business is still in its qualification phase and will likely contribute only minimal revenue this year. |

|||||||||||||||||

→ See also: 70+% Upside Potential: KGI Initiates coverage on PC PARTNER

→ See also: 70+% Upside Potential: KGI Initiates coverage on PC PARTNER