| As the Middle East war saps the strength out of a broad swathe of stocks, investors holding on to significantly shielded businesses are heaving sighs of relief. One such stock is Centurion Corporation, which provides purpose-built accommodation to workers and students in various countries -- Singapore mainly, Malaysia, Australia and the UK. Two analyst reports -- from CGS International and Maybank Securities -- lay out reasons for optimism (more below). Meanwhile, Centurion has recommended a final dividend of 2.0 cents per share, and a special Distribution In Specie of CAREIT units on the basis of one CAREIT unit for every ten Centurion shares held. As illustration: Taking $1.43 and $1.10 as the respective recent trading prices of Centurion and CAREIT, an investor holding 10,000 Centurion shares gets:

|

At Centurion FY25 results briefing: CEO Kong Chee Min (third from left) with (from left): Ho Lip Chin, Chief Investment Officer – Accommodation Business | Foo Ai Huey, CFO | Kelvin Teo, Chief Operating Officer -- Accommodation Business.

At Centurion FY25 results briefing: CEO Kong Chee Min (third from left) with (from left): Ho Lip Chin, Chief Investment Officer – Accommodation Business | Foo Ai Huey, CFO | Kelvin Teo, Chief Operating Officer -- Accommodation Business.

1. Robust Core Profit Growth

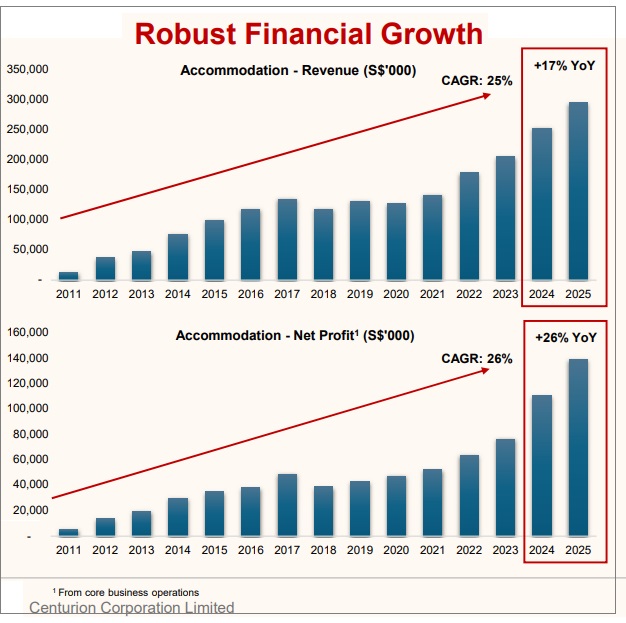

Despite reported net profit being affected by one-off costs, Centurion’s fundamental business remains strong.

In their report titled Building a Growth Story, TAN Jie Hui and William TNG (CGSI) note that "underlying growth was resilient on acquisitions and rental reversions".

They further state, "We expect FY26-28F core net profit to grow 7% p.a., driven by a steady ramp-up of new PBWA and PBSA assets".

2. High Occupancy in Essential Markets

Centurion maintains nearly full occupancy in its primary revenue-generating locations.

In his report titled The Best Is Yet To Come, Eric Ong (Maybank Securities) highlights that this was "driven by healthy rental revisions across key markets and steady occupancies in Singapore and the UK".

CGS analysts point out that while some regions varied, "Singapore remained tight at 99%".

3. Ability to Drive Higher Rents

Centurion has successfully passed on price increases to tenants.

The Maybank analyst observed "continued positive rental rate revisions across both PBWA and PBSA segments".

Similarly, CGS mentions that worker accommodation revenue rose significantly "on stronger rental rates".

|

Item |

FY 2025 (S$’000) |

FY 2024 (S$’000) |

Change |

|

Revenue |

295,937 |

253,616 |

▲ 17% |

|

Gross Profit |

226,985 |

195,620 |

▲ 16% |

|

Gross Profit Margin |

77% |

77% |

0pp |

|

Net Profit |

141,598 |

382,636 |

▼ 63% |

|

Net Profit from core business |

139,197 |

110,808 |

▲ 26% |

|

Net Profit Margin from core business |

47% |

44% |

▲ 3pp |

|

Net Profit (Equity holder)1 |

108,557 |

99,272 |

▲ 9% |

1Net Profit (Equity holder) = Profit from core business operations attributable to equity holders, which excludes the 49% interest in ASPRI-Westlite Papan and Centurion CityhomeXiamen and 57.07% interest in CAREIT

4. Significant New Capacity Coming Online

A steady stream of new beds will provide clear revenue visibility.

CGS identifies "key contributors" such as the "new Westlite Toh Guan block (c.1,764 beds)" and the "Westlite Mandai block (c.3,696 beds)".

Maybank adds that "EPIISOD Macquarie Park, a c.732-bed property in Sydney, has just been completed in 1Q26".

5. Transition to a Profitable "Asset-Light" Model

By managing properties for others and listing its own REIT (CAREIT), Centurion is becoming more efficient.

Eric Ong, the Maybank analyst, explains, "As the group goes asset-light, we reckon CENT will continue to raise its dividend payout".

He further notes the company is seeing "growing recurring fee income along with clear expansion plans".

"We now see Centurion Corporation having three stable, recurring, and very resilient income streams." "We now see Centurion Corporation having three stable, recurring, and very resilient income streams."-- David Phey, Head of Communications, Centurion

|

||||||||||||||||||

6. Beneficiary of Stricter Housing Standards

New government regulations for worker housing act as a barrier to entry for smaller competitors.

CGS analysts argue that efforts "to tightly regulate workers' accommodation standards... bodes well for professional dormitory managers like CENT".

They believe Centurion "can benefit from corporates' growing awareness of the need to improve migrant workers' welfare".

7. Strategic Global Expansion

The company is aggressively looking for new opportunities outside its traditional markets.

Eric Ong notes that Centurion is "exploring development and/or acquisitions... in the Middle East, as well as existing operational key worker accommodations catering to the mining industry in Australia".

8. Compelling Valuation and Upside Analysts believe the stock is priced lower than its actual worth. |

→ See Centurion's FY25 Powerpoint deck here

→ See Centurion's FY25 Powerpoint deck here