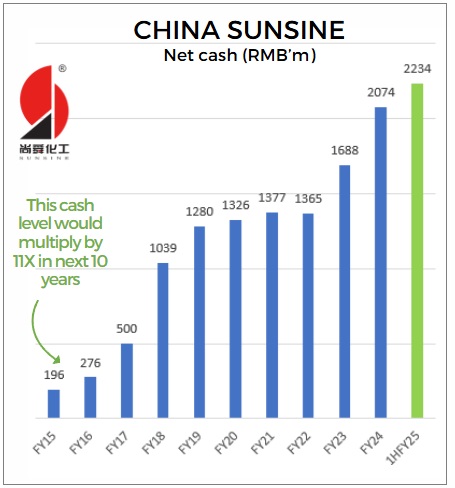

| Singapore-listed since 2007, China Sunsine is cash-rich, growing fast, and has structurally lower costs than its peers. Its exceptionally strong balance sheet shows a huge pile of cash — Rmb2.2bn, in fact.

Established nearly 50 years ago, it has emerged as a global market leader supplying chemicals to over 75% of the top 75 tyre makers. Its ongoing capacity expansion will drive further sales growth from next year. Recently, after visiting Sunsine facilities in Shandong, China, CGS International and UOB KayHian analysts see its future as being bright as the company cement fundamentals for more profit growth. But they also note a current issue -- persistent downward pressure on Average Selling Prices. |

||||

• Market leader poised to benefit from industry consolidation. • Key Drivers: Capacity expansion (Shanxian/Weifang) leading to stronger volumes from 2026. • Structural cost advantages via automation and in-house intermediate (MBT) production, delivering RMB 1,800-2,000/tonne cost savings. • Demand tailwinds from China's EV and replacement-tire markets |

Analyst Agreements: Volume and Consolidation

The analysts -- Heidi Mo of UOB KH and Tan Jie Hui and Lim Siew Khee of CGS -- agree that Sunsine is fundamentally sound and about to get much bigger.

1. The Volume Boom: Sunsine’s massive capacity expansion in Shanxian and Weifang is on schedule.

Total annual capacity is expected to hit 272,000 tonnes in 2026, which management expects will lead to a stronger performance.

2. Market Leader Advantage: High entry barriers, especially around hazardous-chemical licensing and strict environmental compliance, are keeping small players out.

Sunsine’s compliance and valuable waste management licenses give them a competitive edge, so less efficient producers are at risk of being eliminated.

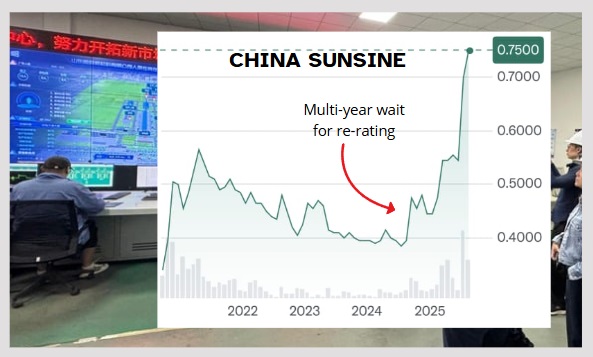

3. Cheap, Cheap, Cheap: Even with current market price pressures, the analysts highlight the stock's low valuation when you strip out the cash.

UOBKH calls the stock attractive at 5x ex-cash 2026F PE, while CGS notes the stock trades at 4.2x P/E on an ex-cash basis.

While UOBKH maintained its BUY rating and set a target price of S$0.95, the CGS analysts did not have a target in their non-rated report (likely because this is their first on Sunsine):

- UOBKH: A re-rating catalyst is management confidence in its earnings visibility, specifically signaled by the formal adoption of a minimum 40% dividend payout policy for FY25 and FY26, paid semi-annually.

Heidi Mo, analystThis exceeds the group’s historical high payout of 36% in 2024.

Heidi Mo, analystThis exceeds the group’s historical high payout of 36% in 2024.

Thus, UOBKH raised its valuation multiple to 11x 2026F earnings, positioning it at +2SD (two standard deviations) above the mean PE. - CGS: Its report focuses on hard operational facts, emphasising Sunsine's structural cost advantages.

Tan Jie Hui, analystSpecifically, new in-house intermediate (MBT) production capacity (60ktpa at Hengshun, 20ktpa at Weifang) is expected to deliver massive cost savings of RMB 1,800-2,000 per tonne.

Tan Jie Hui, analystSpecifically, new in-house intermediate (MBT) production capacity (60ktpa at Hengshun, 20ktpa at Weifang) is expected to deliver massive cost savings of RMB 1,800-2,000 per tonne.

Plus, automation means the company boosted output by 25% over five years without expanding headcount.

For CGS, it's about superior manufacturing execution leading to an earnings rebound.

The current challenge that both reports acknowledge is the industry-wide softness in Average Selling Prices. UOBKH, despite trimming its 2025 revenue forecast by 7% due to this “more subdued ASP environment”, still hiked the valuation multiple to 11x PE. |

→ See the full CGS and UOB KH reports.

→ See the full CGS and UOB KH reports.

→ See also: This Company Raises Minimum Dividend Payout Ratio to 40% Amid Strong Cash Accumulation. How Did It Get Here?