|

The bond market feels like it’s “heating” up in Singapore. Just a few months after retail investors first gained investment access into private equity bonds, comes another first, Temasek’s T2023-S$ bond aimed at both institutional and retail investors in Singapore. |

Here are 7 things we should know about Temasek Holdings’ T2023-S$ bonds before investing in it.

#1 What is up with its Name?

All of Temasek’s bonds are named this way.

T is probably for Temasek, the next four digits represent the year that the bond is maturing (2023), and the currency it is issued in is highlighted at the back (Singapore dollars or S$).

# 2 What Exactly Is The T2023-S$ Bond?

|

"The T2023-S$ is the first time that Temasek Holdings is issuing bonds to retail investors since it started issuing bonds in 2005." |

Most pertinently, the T2023-S$ is the first time that Temasek Holdings is issuing bonds to retail investors since it started issuing bonds in 2005.

A total offer of $400 million will be split evenly between both retail investors and placements to institutional, accredited and other specified investors. This means at least $200 million will be set aside for retail demand. If there is higher demand or an over-subscription, the total offer size could increase to $500 million.

As highlighted, the T2023-S$ bond is a five-year bond, denominated in Singapore dollars, paying a fixed coupon rate of 2.7% per annum.

Allowing for greater liquidity and smaller investment sizes, of as little as $1,000, these bonds will also be listed on the Singapore Exchange (SGX).

|

Coupon |

2.70% per year (fixed coupon), payable every six months |

|

Tenor |

5-years |

|

Issuer |

Temasek Financial (IV) Private Limited, a wholly-owned subsidiary of Temasek |

|

Maturity Date |

Expected to be Wednesday, 25 October 2023 |

|

First Interest Payment Date |

Expected to be Tuesday, 25 April 2019 |

|

Guarantor |

Temasek Holdings (Private) Limited (Temasek) |

|

Offer size |

Up to $400 million, subject to upsize to $500 million Placement: $200 million to institutional, accredited and other specified investors Public Offer: up to $200 million to retail investors in Singapore |

|

Issue Price |

$1 |

|

Minimum Application |

Placement: $250,000, or higher amounts in multiples of $250,000 Public Offer: $1,000, or higher amounts in multiples of $1,000 |

Source: Temasek Holdings

# 3 Why Is Temasek Offering This Bond To Retail Investors?

In May 2016, the Monetary Authority of Singapore (MAS) introduced two new regulations – the Bond Seasoning Framework and the Exempt Bond Issuer Framework – to make it easier for corporate bonds to be issued in Singapore. This could be one reason why Temasek Holdings could be leading the way to offer more corporate bonds to retail investors.

In recent years, different types of bonds have also been introduced to retail investors. This may be to develop the bonds market in Singapore or ensure that retail investors have sufficient choices to make bond investments. The most recent bond-types offered to retail investors include the Singapore Savings Bonds (SSB) in October 2015, the Astrea IV PE Bonds in June 2018 and the Nikko AM SGD Investment Grade Corporate Bond Fund in August 2018.

Lastly, Temasek is a Singaporean brand. By offering its bonds to retail investors in Singapore, it can broaden its stakeholder base in the country and engage them better.

# 4 How Did It Arrive At The 2.7% Interest Rate Return?

The T2023-S$ interest rate was determined via its book building exercise with institutional, accredited and other specified investors. This means that retail investors are receiving interest rates that have already been deemed fair by savvier investors.

Best of all, even though institutional, accredited and other specified investors have to invest a minimum of $250,000, retail investors, who can invest from as little as $1,000, are offered the same interest rate.

# 5 How Does The Interest Return Compare To Other Similar Bond Types?

Given the numerous bond options in the market, including the Singapore Savings Bond, Singapore Government Securities, and other triple-A rated bonds, let’s see how the interest rates compare:

|

Bonds |

Estimated Returns |

|

T2023-S$ |

2.70% p.a. |

|

Singapore Savings Bonds |

2.48% p.a. (Nov 2018 issue if you hold for 10 years); 2.22% p.a. (Nov 2018 issue if you hold for 5 years) |

|

ABF Singapore Bond Index Fund |

2.44% (no maturity period) |

|

CPF Ordinary Account CPF Special Account |

2.50% (only for comparison) 4.00% (transferring into CPF Special Account is a one-way process) |

|

Singapore Government Securities |

1.88% (2-year bond) |

|

Fixed Deposits |

1.80% (36-month fixed deposit at Maybank) |

Based on other similar virtually risk-free investments, the T2023-S$ bonds offer one of the best returns we can get.

However, we also have to note that these bonds will be listed on the SGX. This means that if we want to cash out it before its 5-year maturity period, we have to sell it on SGX, at market prices.

While this is similar to many other listed and unlisted bonds and bond ETFs, this is unlike the Singapore Savings Bonds, which allow us to redeem at any point without any risk of losing our principal. This is also perhaps why the T2023-S$ is paying a better interest return than the Singapore Savings Bonds.

# 6 What Are The Risks Involved?

As mentioned above, the T2023-S$ bonds are delivering the highest interest returns against comparable investment vehicles. As higher returns usually equate to higher risks, we need to understand the risks that we are taking.

Source: Temasek

For most bonds, the default risk of the company is most important, as we want to see our principal paid back at the end of the tenor. As the T2023-S$ bonds are backed by Temasek, a triple-A rated company, and have been given triple-A credit ratings by both Moody’s and Standard & Poor’s, we can take it as a risk-free investment.

Some other risks we need to note include the interest rate environment, which has seen interest rates steadily ticking upwards. We also need to note that when interest rates rise, bond prices tend to fall. If we need to sell the bonds in such situations, we may face losses.

We also have to determine other types of risks before investing, this may include liquidity risks, as it will be listed on the SGX and trading volumes may represent whether we are able to sell the bonds quickly. We also need to decide if we are comfortable with the 2.7% return, as any spike in inflation in the economy could see our real return diminishing. Reinvestment risk is another consideration – whether we may be able to reinvest the coupons paid out every six months at equally attractive interest rates.

# 7 How Can I Invest In The T2023-S$

Of course, we’re all interest to know how to invest in the T2023-S$. Before we even think of subscribing for the T2023-S$, we need to have a CDP account, linked to our bank account with either DBS/POSB, OCBC or UOB. This will allow us to subscribe for it via three methods:

- ATMs of DBS/POSB; OCBC; or UOB

- ibanking or internet banking from DBS/POSB; OCBC; or UOB

- mbanking or mobile banking from DBS/POSB

Source: Temasek

Ensure you have your CDP account number when you are applying via any of the three methods.

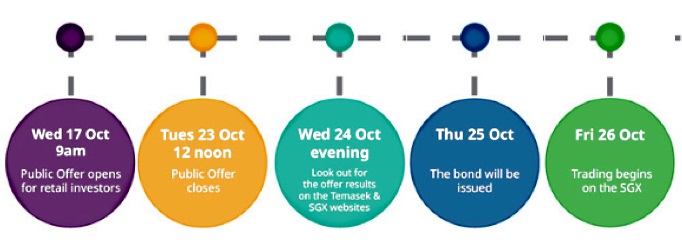

Here’s the timetable of important dates we need to note if you want to subscribe to the T2023-S$ bonds.

|

No. |

Important Dates To remember |

|

|

i |

17 October 2018 at 9am |

The public offer opens |

|

ii |

23 October 2018 at 12 noon |

The public offer closes |

|

iii |

24 October 2018 in the evening |

The offer results will be out on the Temasek and SGX website |

|

iv |

24 October 2018 |

Refunds will be made for invalid and partially successful applicants |

|

v |

25 October 2018 |

Your T2023-S$ bonds will be issued. You can check your CDP account by then. |

|

vi |

26 October 2018 |

T2023-S$ bonds will begin trading on SGX. |

Source: Temasek

Of course, when it’s listed on the SGX, we also need a brokerage account to be able to sell it.

| One Way to Arbitrage the T2023-S$ Bonds |

|

We are able to invest in the T2023-S$ bonds via our CPFIS-OA (CPF Investment Scheme-Ordinary Account), but not our Supplementary Retirement Scheme (SRS).

|

This article is republished with permission from Dollars and Sense.