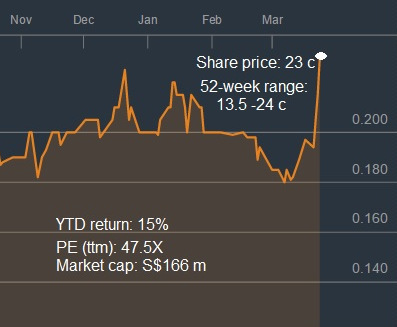

Data & chart: BloombergKINGBOARD COPPER FOIL: This illiquid counter has been attracting attention lately.

Data & chart: BloombergKINGBOARD COPPER FOIL: This illiquid counter has been attracting attention lately.

There's a long-drawn legal dispute dating back to 2011 filed by shareholder Annuity & Re Life Ltd over minority oppression, failing to consider minority shareholders' interest for all actions, failure to pay dividend, disadvantaging the minority via unacceptable transfer pricing, thus favoring the parent.

| In its latest ruling, the Bermuda Supreme Court found that, "as the majority shareholders failed to promptly initiate negotiations with minority shareholders with a view to resolving the impasse and take into account the interests of shareholders as a whole following the blocking of the IPT Mandate, the License Agreement was a commercially prejudicial means of enabling the Company to circumvent the Petitioner’s legitimate exercise of its right to veto the IPT Mandate." (Source: Company announcement dated 12 Nov 2015). In the latest announcement, also reported by The Edge, the Bermuda Supreme Court ordered Kingboard to redeem the shares held by Annuity & Re Life as well as accord the same terms to all current minority shareholders. The terms and conditions of redemption have not been determined, and a hearing has been fixed for 21 April 2016 to determine the legal principles governing a valuation of the shares. |

Depending on the applicable legal principles as determined by the Court, a further hearing may be required to determine the share valuation.

Minority shareholders have been complaining that the process is taking too long and want an ultimatum as soon as possible.

SGX is on top of this whole saga and, certainly, I would like SGX to take a hard stand on the whole issue.

Kingboard Copper Foil's parent, Kingboard Chemical Holdings, listed in Hongkong, has 64.6% of Kingboard Copper Foil shares.

The redemption, if any, may trigger a mandatory general offer under the Takeover Code.

| “Shareholders should further note that the Order and the hearing fixed for 21 April 2016 are proceedings that are taking place in parallel with the appeal filed by the majority shareholders in respect of the judgment of the Court, and that such proceedings may be affected by the appeal process or the outcome of the appeal. While the precise date of the appeal hearing is to be fixed, the Company understands the appeal will take place in March 2017.” -- Kingboard Copper Foil Holdings (18 March 2016) |

The legal struggle is really unnecessary, if Kingboard Chemical agrees to settle the dispute via a privatisation route.

There are 6,700 shareholders on the register, and the valuation offer must be attractive enough to obtain more than 90% acceptance.

Its IPO price in the old days was 53 cents SGD, so anything around that level may garner sufficient acceptance to privatise the company.

Using the exchange rate of S$1 = HK$5.7, its (1) NAV per share: HK$3.789 (S$0.66); (2) Cash balance per share: HK$2.00 (S$0.35), and (3) Net Working Capital per share: HK$2.08 (S$0.36).

All eyes are now on how the valuation and redemption take shape. Prior to his retirement, Chan Kit Whye (left) worked more than 30 years as Regional Finance Director, Financial Controller and Manager in a multinational specialty chemical business. He has played an active role in CPA (Australia) Singapore Branch, taking up positions in its Continuing Professional Development and Social Committees. Kit Whye is a Fellow of CPA Australia, CA of Institute of Singapore Chartered Accountants and CA of the Malaysian Institute of Accountants. He holds a BBus(Transport) Degree from RMIT, MAcc Degree from Charles Sturt University and MBA from Durham Business School.

Prior to his retirement, Chan Kit Whye (left) worked more than 30 years as Regional Finance Director, Financial Controller and Manager in a multinational specialty chemical business. He has played an active role in CPA (Australia) Singapore Branch, taking up positions in its Continuing Professional Development and Social Committees. Kit Whye is a Fellow of CPA Australia, CA of Institute of Singapore Chartered Accountants and CA of the Malaysian Institute of Accountants. He holds a BBus(Transport) Degree from RMIT, MAcc Degree from Charles Sturt University and MBA from Durham Business School.

| ♦ THE FLIP SIDE |

As far as the Board is concerned, the Licensing Agreement was not used as a means of circumventing the veto by shareholders of the renewal of the IPT Mandate. As previously announced by the Company, as a result of minority shareholders voting down the renewal of the IPT Mandate, the management of the Company, in spite of their best efforts, were not able to find customers to whom they are able to supply the same amount of copper foil as they had previously supplied to the Kingboard Group. Accordingly, the Company had entered into the Licensing Agreement with Harvest Resource in order to ensure that a steady stream of income is received by the Company. Harvest Resource was selected to be the licensee as it offered the Company the best terms amongst the other potential licensees. The Licensing Agreement with Harvest Resource was subsequently extended on 30 August 2013 and 28 August 2015, and the Board was satisfied with Harvest Resource’s performance under the Licensing Agreement. In this regard, it should be noted that even though the Court found that “[t]he transaction was in a general sense commercially prejudicial to the Petitioner as a minority shareholder”, the Court had accepted the evidence of Mr. Fanshaw Tan, a Chartered Financial Analyst who gave evidence as a valuation expert for the respondents, that the Company’s opportunities for diversification are hampered by the market reality as “major market players are often vertically integrated [like the Kingboard Group] and often find themselves heavily dependent on their ‘internal’ supplier, through a stable supplier customer relationship”. The Court also inferred from Mr. Tan’s evidence as a whole that the Licensing Agreement was “a response to a crisis which mitigated the far worse damage which might have been suffered by the Company if it had simply lost its major customer and not taken any immediate steps to fill the void.” As stated in the Company’s circular dated 6 April 2011, the Company had not been able to meaningfully diversify its sales to customers outside the Kingboard Group as, among other reasons, the Kingboard Group is the parent group of the Company, and as such, the Company is viewed as a competitor to the potential customers of the Company (namely other laminate manufacturers) who are thus not willing to purchase copper foil from the Company. The Company had successfully increased its sales to third party customers (i.e. customers who are not within the Kingboard Group) from approximately 6.13 per cent. in FY2000, being the first completed financial year after the Company was listed on the Main Board of the SGXST in 1999, to approximately 11.11 per cent. in FY2010. In monetary terms, the revenue attributable to sales to third party customers had increased from approximately HKD24.2 million in FY2000 to approximately HKD474.7 million in FY2010, which represented almost a twenty-fold increase in sales to third party customers since the Company was listed. -- Company announcement dated 22 Jan 2016. |