|

|

New oil company focused on old wells. Giken Sakata (Giken) owns 51% of Cepu Sakti Energy Pte Ltd (CSE), which has signed contracts for five oilfields under Indonesia’s old wells programme. The first two have proven and probable (2P) reserves and best estimate of contingent resources (2C) of 7.6m barrels of oil (mmbo) and 3.8mmbo respectively. We expect the next three fields to be larger.

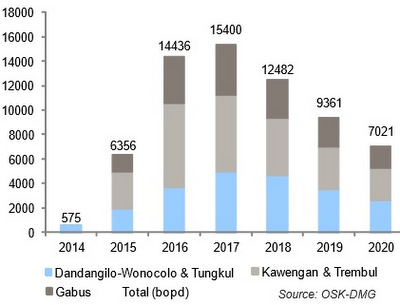

Production expected to surge to 15,400bopd in 2017 from 575bopd

Production expected to surge to 15,400bopd in 2017 from 575bopdin 2014 Superior economics yield NPV/barrel (bbl) of USD16.60/bbl, low oil price variability. The Old Wells Programme has a much simpler cash waterfall that results in an NPV/bbl of USD16.60/bbl vs USD7-10/bbl under production sharing contracts (PSCs). The oil is sold at a fixed price to Pertamina, ie there is almost no oil price risk.

Business model is scalable at negligible cost, strong production ramp-up. CSE can secure new acreages at low cost, requiring only the signing of new contracts. Exploration risk is negligible, as the fields have produced before.

Sydney Yeung, CEO of Giken Sakata. NextInsight file photo.It can even reach first oil in the year of contract signing, with no data acquisition costs. Drilling costs are also <20% of its peers. From c.900bbls of oil per day (bopd) currently, we expect 6,356bopd/14,336bopd in FY15/FY16F.

Sydney Yeung, CEO of Giken Sakata. NextInsight file photo.It can even reach first oil in the year of contract signing, with no data acquisition costs. Drilling costs are also <20% of its peers. From c.900bbls of oil per day (bopd) currently, we expect 6,356bopd/14,336bopd in FY15/FY16F. Strong profitability and cashflow. CSE was already profitable in 1Q14, producing c.300bopd. With a strong production profile, we expect earnings and cash flows to surge.

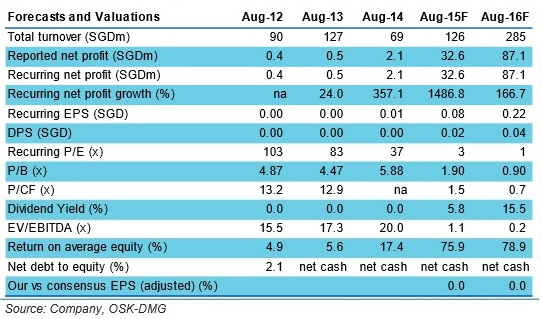

Giken is effectively trading at 3x FY15F P/E, with 1.1x EV/EBITDA. If management pays out 20% of earnings, the yield would be 5.8%/15.5% for FY15/16F respectively.

Deeply undervalued even after price surge. Share prices have surged post acquisition, but market clearly values only two out of its five fields. Our SGD0.65 valuation is based on a DCF of the five fields, which can still grow as it continues to sign more old wells acreage in the Cepu area.

Key risks: Operational delay which may defer production growth; Short track record for CSE; Portfolio concentration.

Full report here.

Recent stories:

GIKEN SAKATA: New Indonesian onshore oil field play

GIKEN SAKATA: To boost earnings with oil & gas drilling