THE EDGE SINGAPORE weekly, in its issue 17 – 23 Sep 2012, had outlined charts for some oil and gas stocks such as Ezion, Kreuz, Ezra, Nam Cheong etc.

I would like to bring readers’ attention to Swiber whose chart looks interesting.

Based on Chart 1 below, Swiber is forming higher highs and higher lows.

It seems to be consolidating around the region of $0.640-0.655 at the moment.

Open balance volume or OBV which incorporates volume to price changes (to detect momentum) is almost near an all time high.

ADX is at 43 with DI positively placed (i.e indicating the presence of a trend).

Supports are at $0.625 / $0.635 / $0.645 and resistances are at $0.675 & 0.695. A more significant resistance lies around $0.705-0.715.

Laggard among oil and gas stocks

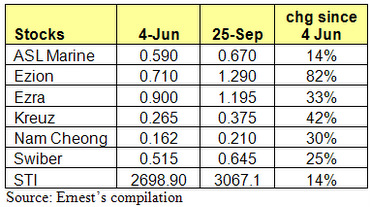

Based on Chart 1 above and Table 1 on the right, Swiber has risen a whopping 25% from $0.515 on 4 Jun to $0.645 on 25 Sep.

However, this pales in comparison to its peers. For example, Ezion and Kreuz have rallied 82% and 33%, respectively since 4 Jun 12.

It is also noteworthy that Swiber announced significant contracts during this period which may have contributed to its rally to a certain extent. (i.e without the contract wins, Swiber’s share price may have climbed to a lesser extent).

Record order books of US$1.6b underpins earnings

As at Aug 2012, Swiber has about US$1.6b of orders with an estimated US$1.0b from new contract wins awarded year to date.

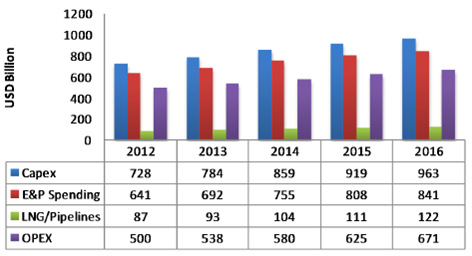

According to Table 2 below, Capex and Operating expenditure (“Opex”) are expected to reach a record US$728b and US$500b respectively in 2012.

This would further rise to US$963b and US$671b respectively in 2016.

Among the regions, Asia Pacific and Middle East are key growth regions with a compound annual growth rate of 7.9% and 8.4% respectively between 2012 to 2016.

Swiber has presence in both of these regions.

Kreuz rise does benefit Swiber

Based on Swiber’s 2011 annual report, Swiber owns 63.2% of Kreuz. As of 25 Sep, after Kreuz’s meteoric 42% rise in three months, Kreuz’s market capitalization is around $209m.

Swiber’s market capitalization is around $393m, of which one third is attributable to Kreuz. In other words, Swiber’s business (ex Kreuz) is only worth approximately S$261m.

Some noteworthy points though…

Redemptions of notes and bonds

With reference to its 1HFY12 results, it is noteworthy that Swiber faces the redemption of its multicurrency medium term notes series 7 & 10, amounting to US$170m in 2HFY12.

In addition, Swiber’s US$100m convertible bond notes may be redeemed in Oct 2012. As a result, Swiber has been exploring various funding options.

On 25 Sep, Swiber has issued S$80m, 9.75% senior perpetual securities which may be used for the redemption. Going forward, it is likely that Swiber may face higher interest expenses.

Laggard = does not mean it will rise soon or definitely rise

Being a laggard does not mean that it will definitely rise, or rise soon. Furthermore, there may be reasons why the stock is unloved by the market.

Support at $0.620-0.625 crucial – rising trend line

The support at $0.620-0.625, as represented by the rising trend line is important. If Swiber breaks below the rising trend line with volume expansion, it does not bode well for the stock.

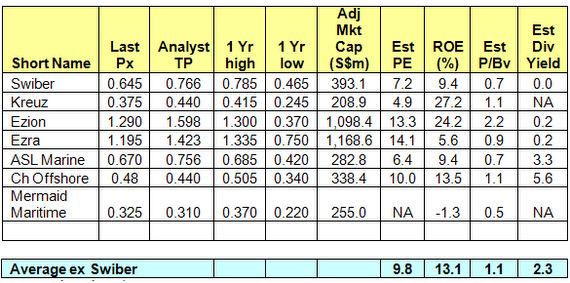

Valuations not excessive against peers

With reference to Table 3 below, Swiber’s valuations do not seem excessive.

Based on its latest 2QFY12 results, Swiber’s NAV / share is around $0.880 and it trades at around 0.7x P/BV.

Its ROE pales in comparison with that of Ezion but if the company can continue to execute on its contracts while keeping costs in check, it is likely that the ROE may be able to improve in the quarters ahead.

P.S: This is just an introduction on Swiber. Readers who are interested in Swiber can email me at

Visit remisier Ernest Lim's blog http://www.ernestlim15.blogspot.com/

Recent articles by Ernest Lim:

NEO GROUP – Delivers the restaurant to you

STX OSV slides despite sale of stake at a likely higher price than market