This article was recently published on Calvin Yeo's blog, www.investinpassiveincome.com, and is reproduced with permission.

AFTER THE Felda IPO, another mega IPO to come from Malaysia is the IHH Healthcare Bhd IPO.

One of the reasons it is particularly interesting is that it will have a dual listing in Singapore and Malaysia, while the primary markets include Singapore, Malaysia and Turkey.

There seems to be a lot of chatter about the many cornerstone investors lined up, including but not limited to EPF, PNB, Blackrock, Singapore GIC etc. So this must be a good deal right? Well, not really. The reason so many huge funds are involved is because of the deal size.

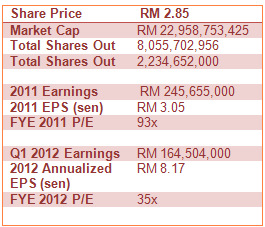

The market capitalization of IHH will be approximately RM 23 billion based on RM 2.85 per share.

One of the reasons why these funds like to go for large deals is their huge fund size and the ability for just one deal to take up a large proportion of their funds as opposed to investing 10 to 30 different companies to make up the same quantum.

Being a Khazanah investment, we will definitely see support from other government institutions such as EPF, PNB, Tabung Haji etc.

Another important aspect is that these funds do not need income from their investments, they are mainly targeting capital growth.

So for individual investors, this may not be that great an investment as they do not have a fixed dividend policy and has not given any hint about what kind of payouts they may adopt. With no dividend yield to work on, I wouldn’t bother investing.

Also looking at use of the proceeds, approximately 90% of the proceeds will be used for repayment of borrowings rather than business expansion.

That’s not a very convincing IPO story. When you look at the pre IPO balance sheet, you will notice that their leverage is rather high at about 47% (Total Liability/Total Assets).

There also seems to be some confusion among various reports on IHH metrics. Looking at the 900-page prospectus, it is easy to see where people got confused. There are 3 groups of financial statements in there -

1. Financials of IHH

2. Financials of Acibadem

3. Pro Forma Financials of IHH + Acibadem

The correct one to focus on should be 3. Pro Forma Financials as you are actually buying the combined entity.

Unfortunately, rather than making it easy to read, the prospectus is often confusing and difficult to digest.

That’s probably why research analysts get paid top dollars!

Hope the table on the left makes more sense. As we can see, trailing P/E is 93x which is very high, compared to Raffles Medical which is only trading at approximately 23x.

Even if we look at forward P/E, it is very high at 35x, compared to Raffles Medical which is only about 21x.

While there is more growth potential for IHH, with projected 3,300 new beds over the next 5 years, there are execution risks.

With such rich valuations, no clear dividend policy and sub optimal use of IPO proceeds, I doubt I will be investing in IHH now.

In fact, healthcare stocks for some reason do not have attractive dividend yields, which explains why none of them are on my portfolio with the exception of healthcare REITs.

Recent story CALVIN YEO: "I'm not interested in low dividend yield of Felda Global'