- Posts: 646

- Thank you received: 1

Inphyy Corner

12 years 5 months ago #18797

by inphyy

Replied by inphyy on topic Inphyy Corner

M1's Q4 net profit up 7.1%

www.businesstimes.com.sg/breaking-news/s...t-profit-71-20140120

Keppel Reit posts 1.97 cent DPU for Q4

www.businesstimes.com.sg/breaking-news/s...cent-dpu-q4-20140120

Jardine Strategic to invest US$731m in HK-listed Zhongsheng

www.businesstimes.com.sg/breaking-news/s...-zhongsheng-20140120

Sembcorp firms boost buyback value

www.businesstimes.com.sg/premium/compani...yback-value-20140120

Osim increases its stake in TWG unit to 70%

www.businesstimes.com.sg/premium/compani...twg-unit-70-20140120

K K Fong's comeback story

Xpress Holdings boss says finding the right model a challenge as he aims to set up at least 100 print stores and shops globally by 2015, reports CAI HAOXIANG

www.businesstimes.com.sg/premium/compani...eback-story-20140120

www.businesstimes.com.sg/breaking-news/s...t-profit-71-20140120

Keppel Reit posts 1.97 cent DPU for Q4

www.businesstimes.com.sg/breaking-news/s...cent-dpu-q4-20140120

Jardine Strategic to invest US$731m in HK-listed Zhongsheng

www.businesstimes.com.sg/breaking-news/s...-zhongsheng-20140120

Sembcorp firms boost buyback value

www.businesstimes.com.sg/premium/compani...yback-value-20140120

Osim increases its stake in TWG unit to 70%

www.businesstimes.com.sg/premium/compani...twg-unit-70-20140120

K K Fong's comeback story

Xpress Holdings boss says finding the right model a challenge as he aims to set up at least 100 print stores and shops globally by 2015, reports CAI HAOXIANG

www.businesstimes.com.sg/premium/compani...eback-story-20140120

Please Log in to join the conversation.

12 years 5 months ago #18798

by inphyy

Replied by inphyy on topic Inphyy Corner

IPO - Kim Heng Offshore & Marine Holdings Limited

Kim Heng Offshore & Marine Holdings Limited ("Kim Heng" or the "Company") is offering 174m shares for the IPO at $0.25 each of which 160m are new shares and 14m are vendor shares. There will only be 3m shares for the public with the balance via placement.

The prospectus is here. The IPO will end on 20 Jan 2014 at 12pm and begin trading on 22 Jan 2014. The market cap post IPO will be around $177.5m. I have two "fact sheets" about the IPO, one from DBSV and one from Lim & Tan for your reference.

Principal Business

Kim Heng has a long history and is an established integrated offshore and marine value chain services provider. The Company offers a one-stop solution for oil & gas projects with customers in more than 25 countries globally.

The Company specializes in offshore rig services and supply chain management as well as vessels sales.(See picture below if you need the details on the business the Company is engaged in).

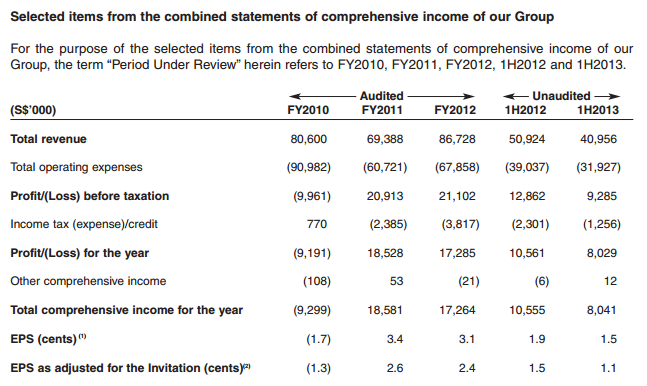

Financial Highlights

The last 3 years figures have been fairly inconsistently with revenue fluctuating and net profit hovering around the 17-18m in the last 2 years. The first half performance also showed a slower pace versus the same period last year. The net profit declined by 24% from the same period last year. As i am not privy to the forward looking results, i can only make a guess.

According to the prospectus, the post invitation share cap is 710m shares and the adjusted EPS for 1H2013 is 1.1 cents. I will assume the full year EPS to be = 1.1 divide by 0.6 (since 1H seemed to be stronger than 2H for FY2012) = 1.8 Singapore cents. Based on the IPO price of 25 cents, the forward PE is around 13.8x.

However according to the fact sheet from Lim & Tan, the Company expects a more robust second half and recommend investors to 'subscribe' for the IPO. Assume a more robust second half, my EPS will be approximately = 1.1/0.4 = Singapore 2.75c and that translate into a forward PE of around 9x (which is reasonable).

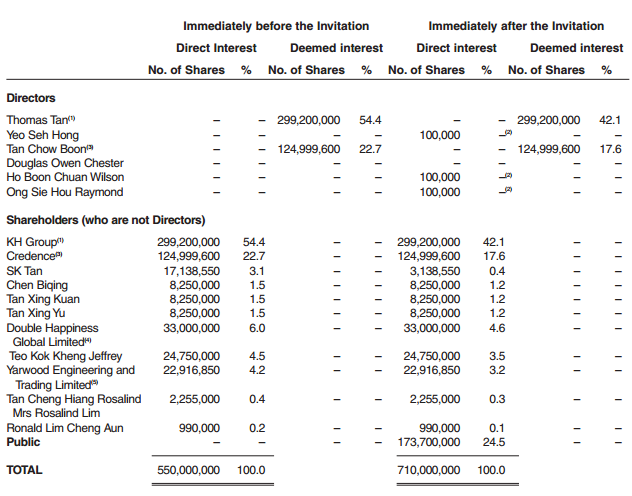

Shareholders

Looking at the list of shareholders, Credence Capital Fund II is run by Tan Chow Boon, Koh Boon Hwee and Seow Kiat Wang and one of the investors of Credence Capital Fund II is Mr. T.

Credence bought into the Company at an average price of 20c. As they invested only in 15 May 2013 and holds a 17.6% stake post IPO, they are still in the value creation mode.Given that it is supposed to generate private equity like returns, Credence's target price to exit will probably be above 40c with a 2-3 years time frame.

What I like about the Company

•Established brand name with more than 40 years track record

•Oil & Gas sector exposure

•Blue chip customers

•Experienced management

•Reputable institutional investors

My Fair Value

Assuming my more "robust" EPS of 2.75c is correct, i will give the IPO a fair value PE range of between 10-12x forward PE and that translate into a price of between 28c to 33c.

My Ratings

I am not privy to any 3 year plan of the Company but i believe Credence will not be there for the short term. As such, i will not give the 1H 2013 results too much weightage. Ms. Syndicate told me that this IPO is very hot and will have a +10c debut. I will tamper that expectation down a bit and say that i believe an opening above 30c is very likely even though the huge placement float of 174m can be a turn off unless they place the shares to institutions and strong hands. If you want to give this a punt, i will say just do it but make sure you apply at least 50-100 lots so that you will get around 3 to 5 lots.

Courtesy of Mr.IPO

singapore-ipos.blogspot.sg/

Kim Heng Offshore & Marine Holdings Limited ("Kim Heng" or the "Company") is offering 174m shares for the IPO at $0.25 each of which 160m are new shares and 14m are vendor shares. There will only be 3m shares for the public with the balance via placement.

The prospectus is here. The IPO will end on 20 Jan 2014 at 12pm and begin trading on 22 Jan 2014. The market cap post IPO will be around $177.5m. I have two "fact sheets" about the IPO, one from DBSV and one from Lim & Tan for your reference.

Principal Business

Kim Heng has a long history and is an established integrated offshore and marine value chain services provider. The Company offers a one-stop solution for oil & gas projects with customers in more than 25 countries globally.

The Company specializes in offshore rig services and supply chain management as well as vessels sales.(See picture below if you need the details on the business the Company is engaged in).

Financial Highlights

The last 3 years figures have been fairly inconsistently with revenue fluctuating and net profit hovering around the 17-18m in the last 2 years. The first half performance also showed a slower pace versus the same period last year. The net profit declined by 24% from the same period last year. As i am not privy to the forward looking results, i can only make a guess.

According to the prospectus, the post invitation share cap is 710m shares and the adjusted EPS for 1H2013 is 1.1 cents. I will assume the full year EPS to be = 1.1 divide by 0.6 (since 1H seemed to be stronger than 2H for FY2012) = 1.8 Singapore cents. Based on the IPO price of 25 cents, the forward PE is around 13.8x.

However according to the fact sheet from Lim & Tan, the Company expects a more robust second half and recommend investors to 'subscribe' for the IPO. Assume a more robust second half, my EPS will be approximately = 1.1/0.4 = Singapore 2.75c and that translate into a forward PE of around 9x (which is reasonable).

Shareholders

Looking at the list of shareholders, Credence Capital Fund II is run by Tan Chow Boon, Koh Boon Hwee and Seow Kiat Wang and one of the investors of Credence Capital Fund II is Mr. T.

Credence bought into the Company at an average price of 20c. As they invested only in 15 May 2013 and holds a 17.6% stake post IPO, they are still in the value creation mode.Given that it is supposed to generate private equity like returns, Credence's target price to exit will probably be above 40c with a 2-3 years time frame.

What I like about the Company

•Established brand name with more than 40 years track record

•Oil & Gas sector exposure

•Blue chip customers

•Experienced management

•Reputable institutional investors

My Fair Value

Assuming my more "robust" EPS of 2.75c is correct, i will give the IPO a fair value PE range of between 10-12x forward PE and that translate into a price of between 28c to 33c.

My Ratings

I am not privy to any 3 year plan of the Company but i believe Credence will not be there for the short term. As such, i will not give the 1H 2013 results too much weightage. Ms. Syndicate told me that this IPO is very hot and will have a +10c debut. I will tamper that expectation down a bit and say that i believe an opening above 30c is very likely even though the huge placement float of 174m can be a turn off unless they place the shares to institutions and strong hands. If you want to give this a punt, i will say just do it but make sure you apply at least 50-100 lots so that you will get around 3 to 5 lots.

Courtesy of Mr.IPO

singapore-ipos.blogspot.sg/

Please Log in to join the conversation.

12 years 5 months ago #18802

by inphyy

Replied by inphyy on topic Inphyy Corner

Centurion Corp to expand Westlite dormitory to 25,000 beds by 2015

Plans unveiled as dormitory officially opens.

Centurion Corporation Limited (Centurion) announced through the Singapore Exchange that it has opened its Westlite Johor Technology Park Dormitory (Westlite), in Senai, Johor, and plans to increase the beds in the dormitory to more than 25,000 by next year.

The purpose-built workers accommodation situated in Jalan Teknologi Johor, opened its doors to foreign workers from the manufacturing sector with a capacity of 5,800 beds.

To our best knowledge, it is also the largest purpose-built workers dormitory being built and managed in Johor thus far.

The development of quality workers accommodation in Johor is expected to help enhance its infrastructure offerings as an attractive destination for multi-national corporations which are looking to set up operations in Malaysia, said Centurion.

These accommodation facilities allow multi-national corporations, especially those in the manufacturing sector, to house their workers conveniently and safely.

This will assist the Malaysian government to control and minimise the social impact of foreign workers living amongst the local communities. In his keynote speech during Westlite's opening ceremony, Datuk Tee highlighted that the Johor Technology Park Dormitory was unlike other dormitories he has seen. “Westlite has built one of the best fully-equipped accommodation for foreign workers.

This dormitory is not just another dormitory; this is the dormitory that will shape and change how dormitories should be, moving forward.

This dormitory, with the facilities that it boasts about, is believed to be the first of its kind in the country,” commented Datuk Tee. The 1.4 hectare project houses a supermarket, grooming salon, food court, medical clinic, gymnasium, media room, fitness centre, sport facilities, as well as internet facilities. “Behind any country’s growth lies the hidden contribution of foreign workers.

It is only fair that we show them our sincere gratitude by providing the best accommodation for them,” added Datuk Tee. Centurion established its first worker accommodation in Tebrau, Johor in 2011 with a bed capacity of 2,500 beds.

It has now grown to five operating worker dormitories with a total bed capacity of 14,400 beds. These worker dormitories are located near key manufacturing hubs across Johor in Desa Cemerlang, Senai, Pasir Gudang and Tebrau.

Two more facilities are currently undergoing development in Tampoi and Senai. To date, Centurion has invested more than RM 80 million in the State of Johor. In addition to the planned expansion by 2015, the Company has also started exploring other regions in Malaysia, outside of Johor. “Our long term vision is to grow our workers accommodation portfolio in Malaysia to as many as 50,000 beds.

We believe this is achievable given the rapid progress Malaysia is making not only in developing its infrastructure but also in attracting foreign direct investments to its shores,” said Mr Kong Chee Min, CEO of Centurion. “We hope Centurion and Westlite can continue being a part of Johor’s impressive growth trajectory,” he added.

Plans unveiled as dormitory officially opens.

Centurion Corporation Limited (Centurion) announced through the Singapore Exchange that it has opened its Westlite Johor Technology Park Dormitory (Westlite), in Senai, Johor, and plans to increase the beds in the dormitory to more than 25,000 by next year.

The purpose-built workers accommodation situated in Jalan Teknologi Johor, opened its doors to foreign workers from the manufacturing sector with a capacity of 5,800 beds.

To our best knowledge, it is also the largest purpose-built workers dormitory being built and managed in Johor thus far.

The development of quality workers accommodation in Johor is expected to help enhance its infrastructure offerings as an attractive destination for multi-national corporations which are looking to set up operations in Malaysia, said Centurion.

These accommodation facilities allow multi-national corporations, especially those in the manufacturing sector, to house their workers conveniently and safely.

This will assist the Malaysian government to control and minimise the social impact of foreign workers living amongst the local communities. In his keynote speech during Westlite's opening ceremony, Datuk Tee highlighted that the Johor Technology Park Dormitory was unlike other dormitories he has seen. “Westlite has built one of the best fully-equipped accommodation for foreign workers.

This dormitory is not just another dormitory; this is the dormitory that will shape and change how dormitories should be, moving forward.

This dormitory, with the facilities that it boasts about, is believed to be the first of its kind in the country,” commented Datuk Tee. The 1.4 hectare project houses a supermarket, grooming salon, food court, medical clinic, gymnasium, media room, fitness centre, sport facilities, as well as internet facilities. “Behind any country’s growth lies the hidden contribution of foreign workers.

It is only fair that we show them our sincere gratitude by providing the best accommodation for them,” added Datuk Tee. Centurion established its first worker accommodation in Tebrau, Johor in 2011 with a bed capacity of 2,500 beds.

It has now grown to five operating worker dormitories with a total bed capacity of 14,400 beds. These worker dormitories are located near key manufacturing hubs across Johor in Desa Cemerlang, Senai, Pasir Gudang and Tebrau.

Two more facilities are currently undergoing development in Tampoi and Senai. To date, Centurion has invested more than RM 80 million in the State of Johor. In addition to the planned expansion by 2015, the Company has also started exploring other regions in Malaysia, outside of Johor. “Our long term vision is to grow our workers accommodation portfolio in Malaysia to as many as 50,000 beds.

We believe this is achievable given the rapid progress Malaysia is making not only in developing its infrastructure but also in attracting foreign direct investments to its shores,” said Mr Kong Chee Min, CEO of Centurion. “We hope Centurion and Westlite can continue being a part of Johor’s impressive growth trajectory,” he added.

Please Log in to join the conversation.

12 years 5 months ago #18805

by inphyy

Replied by inphyy on topic Inphyy Corner

M1 Ltd Dials Up Growth for the Year

By James Yeo - January 21, 2014

Telecommunications provider M1 Limited (SGX: B2F) reported its annual financial results yesterday just after the market closed.

For the whole of 2013, the company saw a 6.3% gain in service revenue from S$772m a year ago to S$820m, helped by higher mobile services and fixed services. However, overall operating revenue actually fell 6.4% year-on-year to S$1.01b primarily due to the steep 38.4% decline in handset sales compared to a year ago.

Nevertheless, its net profit after tax edged up 9.4% year-on-year to S$160m, mainly due to the considerable reduction of operating expenses by 8.6% from S$888.6m to S$812.4m. The curtailment of taxation costs also played an important role by slashing S$4.3m off total expenses, when it decreased from S$36.9m to S$32.6m.

M1’s latest financials showed that it remained in a healthy financial position. Compared to a year ago, its cash & cash equivalents swelled 369.8% from S$11.6m to S$54.5m while its net debt (total debt minus total cash) decreased significantly by 24.9% from S$260.4m to S$195.5m on a year-on-year basis. As a result, its net assets per share increased by 12.3% from 38.1 cents to 42.8 cents as compared to the previous year.

M1 grew its post-paid mobile customer base from 1.095m customers a year ago to 1.13m. It was the fourth consecutive quarterly increase in customer base numbers since the fourth quarter of 2012 for the segment. Elsewhere, its quarterly pre-paid mobile customer base numbers did not fare so well, dropping 3.5% year-on-year to 979,000.

Let’s zoom in to M1′s customer statistics.

Its mobile customers based on both post-paid and pre-paid segments remained essentially unchanged at a total of 2.11 million customers. Then again, both the postpaid and prepaid monthly average revenue per user (ARPU) saw some marginal declines. Postpaid monthly ARPU fell slightly from S$62.7 to S$61.8 while the prepaid figure had a wider difference as it dropped from S$15.4 to S$14.8. Furthermore, M1 also faced year-on-year declines of 9.3% and 2.1% in ARPU for its fixed services and international call services respectively.

M1 also seems to be facing tough competition from its peers SingTel (SGX: Z74) and Starhub Limited (SGX: CC3) as its market share in the mobile market in Singapore declined from 26.1% a year ago to 25.3%.

M1’s management provided some outlook for its network investments in its earnings release: ”The nationwide rollout of 3G radio network on the 900Mhz spectrum will be completed by end of the first quarter. M1 will also be upgrading its 4G network to LTE-Advanced, which can offer higher throughput speeds of up to 300Mbps, by end of the year. These enhancements will further improve customer experience.”

The company’s chief executive, Ms Karen Kooi, also expressed optimsm about M1’s growth that would be driven by both mobile data and fixed services such as home broadband and Pay-TV. In M1’s press release, Kooi commented: “Mobile data will be driven by customers upgrading their smartphone plans and increasing adoption of smartphones by prepaid customers. Fixed services will benefit from the increasing fibre adoption in both the consumer and enterprise segments. We are well-placed to capitalise on these opportunities.”

Shares of M1 closed at $3.24 on Monday and are selling for 18.6 times trailing earnings. M1 has also recommended a final and special dividend of 7.1 cents each, bringing the full-year payout to 21 Singapore cents (a huge 44% jump from the previous year’s annual payout of 14.6 cents), translating into a dividend yield of 6.5%.

Courtesy of The Motley Fool

By James Yeo - January 21, 2014

Telecommunications provider M1 Limited (SGX: B2F) reported its annual financial results yesterday just after the market closed.

For the whole of 2013, the company saw a 6.3% gain in service revenue from S$772m a year ago to S$820m, helped by higher mobile services and fixed services. However, overall operating revenue actually fell 6.4% year-on-year to S$1.01b primarily due to the steep 38.4% decline in handset sales compared to a year ago.

Nevertheless, its net profit after tax edged up 9.4% year-on-year to S$160m, mainly due to the considerable reduction of operating expenses by 8.6% from S$888.6m to S$812.4m. The curtailment of taxation costs also played an important role by slashing S$4.3m off total expenses, when it decreased from S$36.9m to S$32.6m.

M1’s latest financials showed that it remained in a healthy financial position. Compared to a year ago, its cash & cash equivalents swelled 369.8% from S$11.6m to S$54.5m while its net debt (total debt minus total cash) decreased significantly by 24.9% from S$260.4m to S$195.5m on a year-on-year basis. As a result, its net assets per share increased by 12.3% from 38.1 cents to 42.8 cents as compared to the previous year.

M1 grew its post-paid mobile customer base from 1.095m customers a year ago to 1.13m. It was the fourth consecutive quarterly increase in customer base numbers since the fourth quarter of 2012 for the segment. Elsewhere, its quarterly pre-paid mobile customer base numbers did not fare so well, dropping 3.5% year-on-year to 979,000.

Let’s zoom in to M1′s customer statistics.

Its mobile customers based on both post-paid and pre-paid segments remained essentially unchanged at a total of 2.11 million customers. Then again, both the postpaid and prepaid monthly average revenue per user (ARPU) saw some marginal declines. Postpaid monthly ARPU fell slightly from S$62.7 to S$61.8 while the prepaid figure had a wider difference as it dropped from S$15.4 to S$14.8. Furthermore, M1 also faced year-on-year declines of 9.3% and 2.1% in ARPU for its fixed services and international call services respectively.

M1 also seems to be facing tough competition from its peers SingTel (SGX: Z74) and Starhub Limited (SGX: CC3) as its market share in the mobile market in Singapore declined from 26.1% a year ago to 25.3%.

M1’s management provided some outlook for its network investments in its earnings release: ”The nationwide rollout of 3G radio network on the 900Mhz spectrum will be completed by end of the first quarter. M1 will also be upgrading its 4G network to LTE-Advanced, which can offer higher throughput speeds of up to 300Mbps, by end of the year. These enhancements will further improve customer experience.”

The company’s chief executive, Ms Karen Kooi, also expressed optimsm about M1’s growth that would be driven by both mobile data and fixed services such as home broadband and Pay-TV. In M1’s press release, Kooi commented: “Mobile data will be driven by customers upgrading their smartphone plans and increasing adoption of smartphones by prepaid customers. Fixed services will benefit from the increasing fibre adoption in both the consumer and enterprise segments. We are well-placed to capitalise on these opportunities.”

Shares of M1 closed at $3.24 on Monday and are selling for 18.6 times trailing earnings. M1 has also recommended a final and special dividend of 7.1 cents each, bringing the full-year payout to 21 Singapore cents (a huge 44% jump from the previous year’s annual payout of 14.6 cents), translating into a dividend yield of 6.5%.

Courtesy of The Motley Fool

Please Log in to join the conversation.

12 years 5 months ago #18809

by inphyy

Mapletree Logistics Trust: Strong but priced in

www.ocbcresearch.com/pdf_reports/MLT-140121-OIR.pdf

M1: Declares S$0.07 special dividend

www.ocbcresearch.com/pdf_reports/company/M1-140121-OIR.pdf

First REIT: Ends FY13 with 7.52 S cents DPU

www.ocbcresearch.com/pdf_reports/company...0REIT-140121-OIR.pdf

Replied by inphyy on topic Inphyy Corner

Mapletree Logistics Trust: Strong but priced in

www.ocbcresearch.com/pdf_reports/MLT-140121-OIR.pdf

M1: Declares S$0.07 special dividend

www.ocbcresearch.com/pdf_reports/company/M1-140121-OIR.pdf

First REIT: Ends FY13 with 7.52 S cents DPU

www.ocbcresearch.com/pdf_reports/company...0REIT-140121-OIR.pdf

Please Log in to join the conversation.

12 years 5 months ago #18810

by inphyy

Replied by inphyy on topic Inphyy Corner

SATS nine-month operating data show encouraging growth trends

Flights, cargo and passengers handled all up.

In the third quarter of FY2013-14, the number of flights handled by SATS grew 10.2% to 34,920 and unit services increased by 6.6% year-on-year to 28,620.

Also in the third quarter, cargo throughput was up 1.9% to 384,270 tonnes. Passengers handled rose 4.8% to 11.25 million, driven by higher low-cost carrier traffic.

Gross and unit meals, however, declined 8.0% and 5.7% respectively due mainly to the loss of Qantas’ flights to Europe.

Meamnwhile, adding the third quarter data to get the year-to-date operating data, it was shown that all operating metrics grew in the first nine months of FY2013-14 except for gross and unit meals, which posted 7.3% and 5.6% declines, respectively.

Unit services handled was up 7.8% to 83,140 while flights handled has risen 9.8% to 100,570.

Meanwhile, cargo/mail processed ticked up 2.0% to 1,127,100 tonnes as passengers handled ballooned 7.3% to 32.95 million.

Flights, cargo and passengers handled all up.

In the third quarter of FY2013-14, the number of flights handled by SATS grew 10.2% to 34,920 and unit services increased by 6.6% year-on-year to 28,620.

Also in the third quarter, cargo throughput was up 1.9% to 384,270 tonnes. Passengers handled rose 4.8% to 11.25 million, driven by higher low-cost carrier traffic.

Gross and unit meals, however, declined 8.0% and 5.7% respectively due mainly to the loss of Qantas’ flights to Europe.

Meamnwhile, adding the third quarter data to get the year-to-date operating data, it was shown that all operating metrics grew in the first nine months of FY2013-14 except for gross and unit meals, which posted 7.3% and 5.6% declines, respectively.

Unit services handled was up 7.8% to 83,140 while flights handled has risen 9.8% to 100,570.

Meanwhile, cargo/mail processed ticked up 2.0% to 1,127,100 tonnes as passengers handled ballooned 7.3% to 32.95 million.

Please Log in to join the conversation.

Time to create page: 0.154 seconds