Excerpts from analyst reports...

CREDIT SUISSE: HSBC ‘preferred pick’ amid earnings season

Hong Kong banks will report 1H earnings in August and Credit Suisse says the interim results will not be a major catalyst to share price performance as fundamentals remain unexciting with revenue trend under pressure, and costs and credit costs are on the rise.

“The banking sector underperformed the index by 3%, market cap weighted.

"While recent concerns about tightening of liquidity and increasing regulatory oversight are overdone, we view the sector lacks immediate catalysts for a strong rerating in the near term.”

Credit Suisse added that banks’ outlook should remain sanguine with slower but decent and higher yield lending. Costs and credit costs are expected to further trend up but the impact is expected to be manageable, and capital looks adequate for the sector.

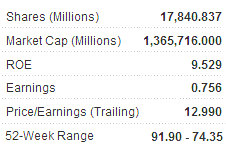

“HSBC (HK: 5) remains our preferred pick into first half results season on strong funding, defensive NIM.

"Bank of East Asia (HK: 23) is our least preferred on sector high cost/income, and increasing credit tightening in Mainland China should impact bank’s profitability.”

Meanwhile, Credit Suisse said that Wing Hung Bank Ltd (HK: 302) is its “preferred pick for medium-cap” on high earnings visibility; with negatives already priced in.

See also: FOCUS MEDIA: Singapore, Hong Kong Ad Firm's HK Placement 20x PE

HAITONG: SA SA kept HOLD on PRC shoppers

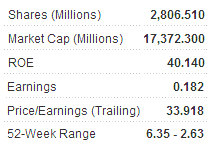

Haitong Securities said it is reiterating its HOLD call (target price: 6.24 hkd) on Sa Sa International Holdings (HK: 178) thanks to the steady and growing flow of Mainland Chinese “tourist shoppers” arriving in Hong Kong.

“Visitor arrivals to Hong Kong reached a record half-yearly high in 1H11 and posted a 14.7% yoy increase to 19 mln. Mainland China remained the main source market, recording robust 20%-plus yoy growth to over 12 mln visitors thanks to the relaxing of the individual visit scheme and the appreciation of the renminbi.”

Haitong said the strong China growth will continue to benefit Sa Sa, as sales to mainland customers remain one of the key generators of its Hong Kong and Macau sales, which accounted for 46% of the total in FY11 (year ending March 31).

Cosmetics and skin care were one of the three most popular shopping categories among overnight visitors in 2010, according to the Hong Kong Tourism Board.

“While the average ticket per transaction for mainland tourists is higher compared to local consumers, the continued buoyant arrivals will drive up both the number of transactions and average ticket per transaction. The favourable Hong Kong environment with its low unemployment rate and steady growth in wages will also boost both variables,” Haitong said.

It added that Sa Sa’s new product and stockholding strategy implemented this year will continue to increase product variety which in turn will attract a wider range of customers.

“We believe the move will also help to increase market share in Hong Kong. In fact, the 1Q12 results demonstrated the positive impact of the strategy with Hong Kong and Macau posting 39% yoy growth in turnover.”

Elsewhere, Haitong said the company is planning to accelerate network expansion in the mainland, which will help increase brand awareness as well as bargaining power and in turn help Sa Sa negotiate better rental rates and locations.

The aggressive store expansion plan to more than double its number of stores during FY11-13 will drive up the top line and improve same-store-sales growth.

See also: YANGZIJIANG, DAIRY FARM, GCL-POLY: What Analysts Now Say...

GUOCO: CHU KONG kept BUY on strong 1H

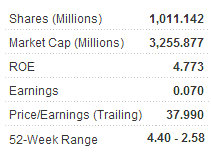

Chu Kong Steel Pipe (HK:1938) saw first half net profit increase 118.7% yoy to 113 mln yuan, earning it a BUY call reiteration from Guoco and a target price of 4.20 hkd.

“CKSP’s earnings recovery was mainly due to strong revenue growth during the period. Revenue increased by 88.7% yoy to 1.6 bln yuan, underpinned by strong growth of sales volume (~80%yoy according to our estimate) and slight improvement of ASP (~5% yoy according to our estimate),” Guoco said.

Gross margin of CKSP slightly declined from 16.9% in 1H10 to 16.5% in 1H11, mainly due to weakening profitability of steel pipes manufacturing services, while gross profit per tonne improved by 2.6% yoy to 1.25 bln yuan in 1H11 and is likely to be higher yoy in 2H11, thanks to greater contribution from higher margin overseas orders and improving operational efficiency.

“We estimate GP/t of LSAW steel pipes to be 1.55 bln yuan, up 14.5% yoy, assuming a stable and efficient cost plus business model. Utilisation rate will be very tight for the rest of 2011, guided by management during recent visit,” Guoco added.

Domestic demand will add more contribution in 2H11, the brokerage said.

“Industry sources reported that PetroChina has planed to build more than 40,000km oil and gas pipelines during the period of 2011-2015. This translates into 16 mln tonnes of steel pipes demand, in our estimate. It is likely that PetroChina would start some projects in 2H11, which might add more contribution to CKSP’s order book in 2H11.”

See also: GALAXY ENTERTAINMENT: Bingo! Up 1,700% In 2.5 Years