Excerpts from CIMB's report this morning....

Analysts: Gary Ng and William Tng

Who else in the water treatment sector may be wooed by private equity or unroll corporate actions? If we have to pick somebody, our water expert sees United Envirotech (UENV) as the most likely candidate. Why?

• Same size as Sinomem. UENV is as big as Sinomem, and as well-known in the water sector.

This company successfully raised NT$500.8m from its secondary listing in Taiwan in Oct 10. When the TDRs were listed, they were trading at twice the price of their SGX counterparts. UENV has also secured Rmb3bn of credit from Chinese bankers for investing in regional membrane-based industrial and municipal wastewater treatment projects.

Would the group consider an M&A with its technology vendor Memstar Technology? With Sinomem sewing a deal with Clean Water Investment Ltd, would other private-equity firms seek out UENV or would UENV emulate Sinomem and get more interested in having dinner with private-equity firms? Only time will tell.

(Of course, we have no answer, but we highlight this, given that this analyst still remembers the time when JIT Holdings, the first contract manufacturer in Singapore to be bought over (by Flextronics) kicked off the M&A wave for the Singapore contract manufacturing sector. Subsequently, Li Xin, a listed mould maker was also bought out by Flextronics as JIT introduced Li Xin to Flextronics. Of course, there were other factors involved then.

• Sound Global: Chairman Wen Yibo takes the plunge with a purchase of 500,000 shares in Sound Global (his first direct on-market purchase since listing in Oct 06). Sound Global has access to opportunities in rural and town project developments in China.

Recycling water is also considered a growing business as well as a good solution to China’s water supply problems. Management strongly believes in the outlook for China’s water sector and the demand for water and wastewater treatment. The group will also continue to expand outside China and speed up its “globalisation”.

• We can’t talk about the water-treatment sector without mentioning Hyflux, the prima donna. We believe its sell-down in recent days was overdone, considering it has already made clear it is beefing up its presence in China (rather than Middle East) in the near term. Its joint venture with Mitsui will spearhead both parties’ ambitions in China, while opportunities for tariff increases in China could boost its O&M income.

Yesterday, Hyflux was named by PUB, Singapore’s national water agency, as the preferred bidder for Tuas seawater desalination plant (one of the catalysts we are looking for) with project cost of the desalination plant and power plant is S$890m. The size of the contract win, in our opinion, will excite the market coming in a time when share price were oversold in the aftermath of MENA unrest.

What our rock-star (analyst) thinks

• Our ever-enthusiastic rock-star analyst rolls the dice and has this to say:

• C&O Pharmaceutical – Chances: High

Company is cash-rich, and paid good dividends in the past. Has had net cash since its listing in FY05, supported by operating cash flows, a product of tighter working-capital control. Recently, Sumitomo took a 29% stake in the company as a strategic investor. Float has dropped to around 30%. Sumitomo could trigger a privatisation if it decides to raise its stake further.

• China Animal Healthcare – Chances: A long shot, but possible

Major shareholders, Blackrock and Fidelity, have upped their stakes substantially in recent months. The company has growth to show and was one of the star S-Chips last year. Having completed its dual listing in Hong Kong late last year, investors will naturally wonder if a de-listing of its Singapore shares may be next.

• Techcomp – Chances: Let’s get through the HK listing first

Techcomp (though not strictly an S-chip) had over the weekend announced dual listing plans in Hong Kong. Management thinks this is desirable so that the company can have ready access to different equity markets when required.

Listing on the SEHK may enhance its profile in Hong Kong and China, facilitate investment by Hong Kong investors, and give it access to Hong Kong's capital markets and a wide range of private & institutional investors. While Singapore-based investors may not have the stomach to re-rate Techcomp, Hong Kong-based investors may.

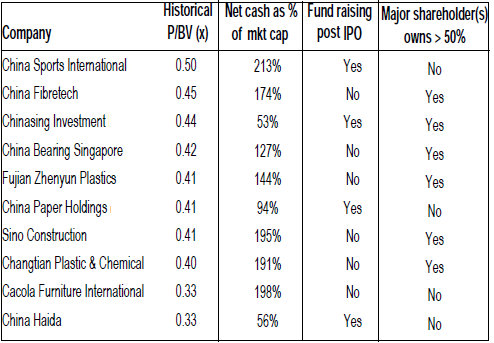

We need a systematic approach to trawl for possible candidates of corporate actions.

I have widened the scope to include those S-chips which may have reasons for attracting the attention of third parties and possible privatisation.

• What would common sense dictate as the criteria for a database search? We think they would be:

1. Trading below book value; we use historical P/BV of 0.5x or less;

2. High net cash as a percentage of market cap; we use more than 50%;

3. Those that have not tapped capital markets since IPO have a stronger reason to de-list; and

4. Those with controlling shareholder(s) with more than a 50% stake will facilitate any potential transaction.