| Much has been highlighted about Vietnam and Russia being core contributors to Food Empire's growth and resilience, respectively. Under a new classification by Singapore-listed Food Empire, it has emerged that Central Asia (driven mainly by Kazakhstan) has been a less-heralded growth compounder. Revenue from the region surged 25.6% to US$102 million in 2025 on double-digit volume growth of its 3-in-1 coffee and the full-year contribution from Tea House LLP. In Kazkhstan, the biggest market in the Central Asia region, Food Empire's MacCoffee brand commands over 70% share of the instant coffee market and significant gross margins.  |

That momentum is about to accelerate.

The group’s new coffee-mix manufacturing facility in Kazakhstan is complete and will commence production in 1Q2026, slashing logistics costs and boosting cash flow by producing locally instead of shipping from Malaysia.

Analyst William Tng of CGS International highlighted the potential: “With its new coffee-mix production facility in Kazakhstan ... there could be incremental earnings upside from Kazakhstan over FY26-28F.”

The same playbook is unfolding in Vietnam.

Southeast Asia revenue rose 14.2% to US$147.8 million last year, led by sustained gains in Vietnam where Food Empire’s coffee-mix market share stood at approximately 17% — despite fierce competition from Nestlé, G7 and local players.

Construction of a new freeze-dried soluble coffee plant in Vietnam started in 4Q2025 and will come on stream by FY2028.

CEO Sudeep, when asked about expansion into China, said "not in the immediate future" as Food Empire is "currently very busy with our existing multiple continents, and there is still potential for double-digit growth there." CEO Sudeep, when asked about expansion into China, said "not in the immediate future" as Food Empire is "currently very busy with our existing multiple continents, and there is still potential for double-digit growth there." |

This multi-continental spread sets Food Empire apart from peers.

While Delfi Ltd. is often cited as a comparable pure-play F&B name on the Singapore Exchange, its chocolate business is concentrated in Indonesia (~60%) and spread across Southeast Asia (mainly Malaysia).

Food Empire, by contrast, draws significant revenue from five distinct geographies:

|

Region |

FY2025 (US$m) |

FY2024 (US$m) |

Change (%) |

|

TOTAL REVENUE |

577.0 |

476.4 |

21.1 |

|

Russia |

191.0 |

141.7 |

34.8 |

|

Southeast Asia |

147.8 |

129.4 |

14.2 |

|

Central Asia |

102.0 |

81.2 |

25.6 |

|

South Asia |

71.0 |

61.4 |

15.6 |

|

Europe |

48.6 |

45.2 |

7.5 |

|

Others |

16.6 |

17.5 |

(5.1) |

Source: Company

That wide geographic reach which confers not only growth potential but also resilience in rough times was further illustrated in a post-earnings briefing where CEO Sudeep highlighted the two coffee plants India as running “fantastically well" at almost 100% capacity, with an ongoing construction of a third plant for a 60% capacity expansion by FY2027.

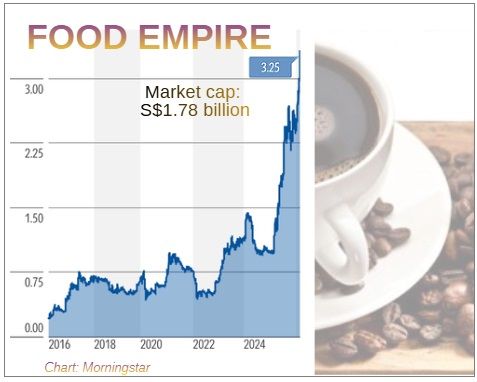

All in, they helped produce Food Empire’s strongest set of results in its 25-year listed history.

Buoyed by these results, the group proposed a record total dividend of S$0.12 per share (FY24: S$0.8 per share).

|

Item |

FY2025 (US$m) |

FY2024 (US$m) |

% Change |

|

Revenue |

576.9 |

476.3 |

21.1 |

|

Operating profit |

93.4 |

63.3 |

47.5 |

|

EBITDA# |

113.5 |

78.3 |

45.0 |

|

Net profit after tax# |

68.6 |

50.0 |

37.0 |

|

Basic EPS (USD cents)# |

12.55 |

9.45 |

32.8 |

|

# normalised: excludes one-off, non-cash, fair value accounting loss on REN amounting to US$32.6 m in Dec 2025 (31 Dec 2024: excludes a fair value accounting gain of US$2.8 m). |

|||

Food Empire had raised S$41.8 million via a placement of treasury shares, ending the year with US$181.6 million in cash after generating US$87.1 million in operating cash flow.

Analysts John Cheong, Heidi Mo and Tang Kai Jie of UOB Kay Hian called the results “solid execution” that “justifies rerating,” raising the house target price 40%, from $3.00 to S$4.21.

“FEH trades at only 19x 2026F PE, a deep 30% discount to regional peers’ average of 27x,” he added.  William of CGS has a S$4.00 target, saying Food Empire “is on the right track to grow its earnings base over FY26-28F. A potential bonus issue in FY26F would also support share price.”

William of CGS has a S$4.00 target, saying Food Empire “is on the right track to grow its earnings base over FY26-28F. A potential bonus issue in FY26F would also support share price.”

Asked about the impact of coffee bean prices which have fallen 20-30% from peaks, CEO Sudeep noted the typical three-to-six-month contract lag but stressed strategic flexibility: “Margins are in our hands.”

Translated: Food Empire has the ability to manage its margins by scaling back or increasing marketing expenses.

Sudeep: "When commodity prices come down, most players reinvest in promotions to pick up volumes that may have suffered when prices were high."

UOB analysts added that “declining coffee prices [will] support margin expansion” in 1H2026, while “capacity expansion underpins long-term growth.”

CafePHO is Food Empire's top-selling product in Vietnam.With new plants in Kazakhstan (2025), India (2027) and Vietnam (2028), market leadership in Central Asia and Russia, and a battle-tested ability to gain market share against the likes of Nestlé and JDE, Food Empire enters FY2026 with multiple engines firing. CafePHO is Food Empire's top-selling product in Vietnam.With new plants in Kazakhstan (2025), India (2027) and Vietnam (2028), market leadership in Central Asia and Russia, and a battle-tested ability to gain market share against the likes of Nestlé and JDE, Food Empire enters FY2026 with multiple engines firing.Even the Russian ruble is looking positive or stable after providing a tailwind in 2025 when the strengthening ruble accounted for roughly US$20 million of the revenue increase. Aside from those factors, Food Empire's balance sheet and brand strength are likely to keep it running fast for years to come. Southeast Asia, in particular, is expected to grow significantly due to the large amount of investment poured into the region. |

→ See Food Empire's FY2025 results Powerpoint deck.

→ See Food Empire's FY2025 results Powerpoint deck.

→ Also: Why CGS Sweetened Food Empire's Target Price to S$4.00