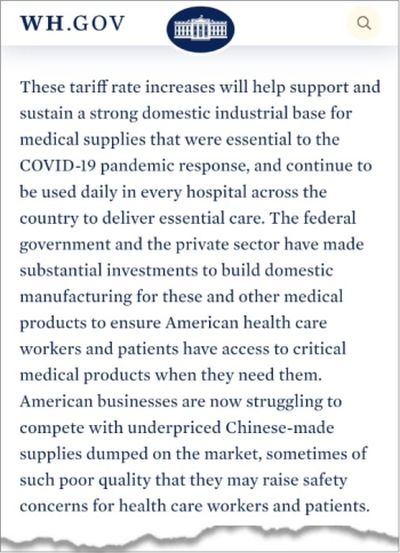

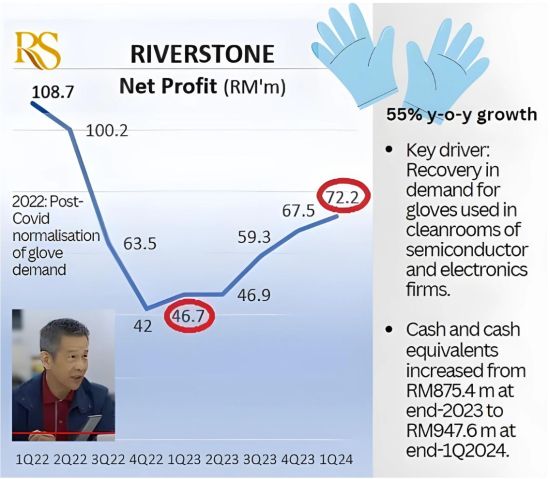

| • Glove-manufacturing is a highly competitive business. Profits have eluded many regional players in recent years. Except for Singapore-listed Riverstone Holdings. • That's why its stock is up 33% so far this year (from 70 cents to 93 cents). And this is after going x-dividend for its FY23 final & special dividends totalling 3.559 cents/share.  • Its trailing PE of 20+ is not cheap. But Riverstone's high dividend payouts coupled with rising profitability and an outstanding cash balance -- these help explain its attraction to investors. Now there's one more on the horizon -- courtesy of US President Joe Biden. He has announced a hike in tariffs on China-made gloves, which is likely to benefit Riverstone's exports (and that of other non-China sources) to the US.  Source: White House press release Source: White House press releaseSee our story Its 1Q profit surged 55%. It continues to outshine its peers and it's got momentum. And read UOB KH's analyst report below.... |

Excerpts from UOB KH report

Analysts: John Cheong & Heidi Mo

Riverstone Holdings (RSTON SP)

| Beneficiary Of US Tariff Hike And Glovemaker With The Most Attractive Valuation; Raise Target Price By 12% Riverstone is set to benefit from the higher US tariffs on China’s gloves as it will ease the competition in the healthcare glove and lower-tier cleanroom glove industries. The US market’s contribution to Riverstone’s total revenue, which was 18% in 2023, could rise when the tariff starts. Riverstone’s 2025 PE of 16.6x is at a 60% discount vs peers’ average of 40.7x and offers a way higher dividend yield of 8% vs peers’ average of 1%. We raise our target price by 12% to S$1.12. Maintain BUY. |

WHAT’S NEW

• Higher US tariffs on China’s medical and surgical gloves from 2026.

|

Riverstone |

|

|

Share price: |

Target: |

US President Joe Biden announced new tariffs on US$18b worth of Chinese imports, including rubber medical and surgical gloves, among others, on Tuesday.

The current 7.5% tariff on China’s glove exports will more than triple to a steep 25% and will take effect from 2026.

• Anticipating a shift in business landscape.

Malaysian glove manufacturers like Riverstone are seeing stiff competition from China peers like Intco Medical and Blue Sail, which ramped up production capacities while lowering production costs to effectively capture market share since the pandemic.

China glove makers currently have competitive ASPs of around US$17/’000 pcs and operate at >90% utilisation rate, as compared to Malaysia glove makers’ higher ASPs of >US$20/’000 pcs and 40-70% utilisation rate.

For Riverstone, the emergence of China players has impacted the demand for its healthcare gloves and the lower tiers of its cleanroom gloves.

• Riverstone to benefit from potential higher US demand.

When the new tariffs kick in, China-made gloves will be more expensive.

As Chinese glove makers lose their price competitiveness, Malaysian glove makers like Riverstone will have an opportunity to increase their exports to the US and regain their market share.

| "Leveraging on its newly added capacities from newer production lines that will be operational by end-24, we anticipate higher utilisation for Riverstone’s manufacturing facilities moving forward." |

To recap, the US contributed RM205.3m or 18.1% of Riverstone’s 2023 revenue. This is 32.5% lower yoy from RM304.1m or 24.1% of revenue in 2022.

Additionally, in 1Q24, Riverstone shared that they saw more demand from US buyers in the healthcare gloves segment, likely for inventory restocking purposes.

Leveraging on its newly added capacities from newer production lines that will be operational by end-24, we anticipate higher utilisation for Riverstone’s manufacturing facilities moving forward.

John Cheong, analyst• Riverstone offers the most attractive valuation in the glove industry with a 60% discount in terms of PE multiple and 8x higher dividend yield vs peers. John Cheong, analyst• Riverstone offers the most attractive valuation in the glove industry with a 60% discount in terms of PE multiple and 8x higher dividend yield vs peers.Riverstone’s 2025 PE of 16.6x is at a 60% discount vs peers’ average of 40.7x and it offers a way more attractive dividend yield of 8% vs peers’ average of 1%. We think Riverstone is a good proxy to the recovery in the healthcare glove industry while offering downside protection given its dominant position in the cleanroom glove sector. |

Full report here