Kingston Securities: CASABLANCA to Boost Capacity 30%

Casablanca CFO Gary Ho (second from right) replies to investors while other executives listen in during a recent meeting in Hong Kong. From left: Vice Chairman and Executive Director Ricky Cheng, CEO and Executive Director Sean Sung and IR Officer Ruby Chan.

Casablanca CFO Gary Ho (second from right) replies to investors while other executives listen in during a recent meeting in Hong Kong. From left: Vice Chairman and Executive Director Ricky Cheng, CEO and Executive Director Sean Sung and IR Officer Ruby Chan.

Photo: Aries Consulting

Kingston Securities is maintaining its “Buy” recommendation on bedding products play Casablanca (HK: 2223) following a 9.8% 2012 revenue jump to 473 million hkd.

Kingston has a 2.5 hkd target price on Casablanca (recent share price: 2.24).

“Casablanca’s Huizhou plant will commence operations in H1 which will raise production capacity by 30%. Also, the firm will gradually complete the installation of POS systems by end-2014, providing sales information in a timely and accurate manner, and improving operational efficiency,” Kingston said.

The brokerage’s buy-in price for Casablanca is 2.2 hkd, with a stop-loss of 2.1.

While Casablanca’s 2012 net profit fell 30.2% to 32.02 million hkd, if listing expenses were excluded, overall net profit would have increased 16.6% to 53.5 million.

Casablanca is recently trading at around 2.24 hkd. Source: Yahoo Finance

Casablanca is recently trading at around 2.24 hkd. Source: Yahoo Finance

GPM and EBITDA margins improved to 61.8% and 15.1%, respectively.

“The Group adopted a multi-brand strategy, targeting different demands in the market. Other than self-owned brands ‘Casablanca’ and ‘Casa Calvin’, the Group renewed licensing agreements with ‘Elle Deco’ for exclusive franchise rights in the PRC, Hong Kong and Macau until 2015,” Kingston added.

Also, satisfactory sales were generated from other international brands including “Tru Trussardi,” “Home Concept,” “Move” and others.

Aggregate revenue of licensed brands grew by 32.9% in 2012 to 82.3 million hkd.

Casablanca is currently at net cash position, with cash of 138 million hkd.

Bocom: CHINA TAIFENG BEDDING 2013 P/E Just 3.2x

Bocom: CHINA TAIFENG BEDDING 2013 P/E Just 3.2x

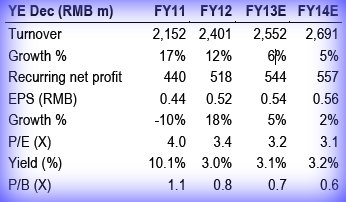

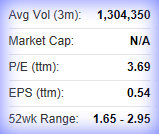

Bocom Research is maintaining its “LT Buy” call on China Taifeng Bedding (HK: 873) with a 2013 P/E of just 3.2 times.

The target price is 2.84 hkd (recent share price 2.17).

Taifeng’s 2012 net profit rose 18% and was 5% above Bocom’s forecast, due to better revenue growth and operating expense ratio.

The segment’s revenue growth was driven by a 31% sales increase to major distributors, even though the number of directly operated stores rose 67% to 865.

The 2012 dividend payout ratio dropped from 40% to 10% although the net cash balance increased 62% to 1.2 billion yuan.

Recently 2.17 hkd“We believe the company is reserving cash for potential big investment in raw cotton processing facilities,” Bocom added.

Recently 2.17 hkd“We believe the company is reserving cash for potential big investment in raw cotton processing facilities,” Bocom added.

Key investment risks include a relatively low visibility of corporate sales by distributors and execution risks from potential high-capex investment.

Investors are also advised to take note of China Taifeng Bedding's relatively high dependence on a few customers and easing growth of the overall bedding products sector.

See also:

CASABLANCA: Newly Listed Bedding Play Eyes Waking Up Mainland Market