Yuanta: China Strategy

Yuanta Research asked the question: “What will drive growth following the 18th National Congress?”

“The Hong Kong Monetary Authority (HKMA) stepped into the currency market on Oct. 19 in order to limit appreciation of the HKD, in line with our view that increasing capital inflows are driving the Hang Seng Index’s (HSI) rebound.

“China’s new cabinet, which will be elected at the18th National Congress (NC), could shift the government’s focus towards growth from domestic demand rather than investment-driven growth,” Yuanta said.

The research note said it believes the PRC economy “will rely on new sources of demand going forward.”

Demand from SOEs

China launched stimulus packages of more than 20 billion yuan from 1Q-3Q12 and as a result, Beijing has opened up previously state-controlled sectors to private investment in order to attract more capital for stimulus projects.

“The state council recently issued guidelines to further encourage private investment in the restructuring of state-owned enterprises and we believe state-owned enterprises could drive the next round of growth in China.

Demand from China’s New Middle Class

China’s new middle class is expanding rapidly (annual income above 100,000 yuan).

“We believe the new middle class will be major consumption growth drivers going forward, with the travel, food and social networking related sectors likely to see increased demand,” Yuanta said.

The research note said new sectors would drive growth.

“With the economy bottoming out, government policies suggest that the real estate and auto industries will no longer be catalysts for economic growth. Consequently, demand for building materials, home appliances and raw materials will slow.

“Meanwhile, overcapacity caused by excessive investment in the past will continue to drag on the steel, solar energy and shipbuilding industries. We believe emerging industries supported by the new government and high-end consumer products will see strong growth going forward.”

Yuanta said it is most positive on the consumer, telecom, shale gas and railway sectors.

Credit Suisse: China Market Strategy

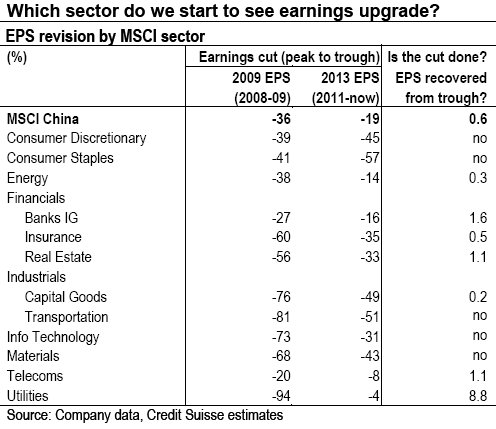

Credit Suisse asked the question: “Is the earnings downgrade cycle over in China?”

“The MSCI China EPS for 2013 has been cut by 20% since May 2011 and after 16 months, we started seeing stabilization in September, followed by minor upgrades in October.

“We see this as a positive based on our experience in 2008/09 when the market in fact bottomed six months ahead of the earnings cycle,” CS said.

The research note added that even if the downgrade is not done and we see another round of earnings cuts, CS does not expect it to be as large as the previous cycle, and the market will probably not react to further downgrades.

“Besides, we see valuation support on the downside when the 25% EPS cut will bring P/E back only to the long-term average.”

Looking into individual sectors, CS said it has started seeing EPS downgrades completed followed by minor upgrades in utilities, banks, property and telecoms.

In 2008 MSCI China troughed in October when earnings did not bottom until six months later.

During then (October 08 to April 09), the 12M EPS further corrected by 20%, while the market rallied over 60%.

MSCI China is trading at 9.5x forward P/E, which is 0.75 SD below the long-term average.

“Even if we see another round of earnings cuts of 25%, which we think is unlikely, the valuation is only back to its long term average. Therefore, we see limited downside from here.

“As for EPS cuts for each sector during the two cycles, the cuts in consumers are more severe in this cycle, whereas those in the telecoms and utilities sectors are more resilient.

“On the other hand, we started seeing downgrades completed followed by minor upgrades in sectors like utilities, banks, property and telecoms,” CS said.

JP Morgan: Moderate China Recovery on Way

JP Morgan said that judging by the October flash PMI improving to 49.1, it sees a “moderate recovery” in China on the way.

China’s flash reading for October manufacturing PMI increased for the second month, rising to 49.1 (J.P.Morgan: 48.5) from 47.9 in September. The improvement is broad-based.

Photo: Centaline

Moderate Recovery on Way

Overall, the improvement in the October flash PMI reading suggests that the manufacturing activities continued to recover this month.

“This reflects the impact of policy easing that has accelerated since May, including pick- up in infrastructure investment, fiscal expenditure, accommodative liquidity condition and monetary policy stance.

“In addition, stabilization in the housing market in recent months has also provided support to domestic demand,” JP Morgan said.

Nonetheless, the research note said weakness in the manufacturing sector and a fragile external environment remain the biggest risks on the road to economic recovery.

“On the policy front, we expect that the government will continue the policy easing measures at a similar pace, so as to ensure the firming up of the recovery process. However, the likelihood of significant pushup in stimulus measures is small,” the research house added.

JP Morgan expects no further rate cuts and one more RRR cut for the rest of the year.

“Overall, we expect that 4Q GDP growth to come in at 8.2% q/q, (vs. 7.1% q/q, in 2Q and 7.7% q/q, in 3Q). In year-over-year term, GDP growth is likely to stay unchanged in 4Q at 7.4%. Our full-year GDP forecast remains unchanged at 7.6% in 2012.”

Deutsche Bank: Property Tour Takeaways

Deutsche Bank said it recently visited various residential/retail projects in Shenyang – a major industrial city in Northeastern China with nearly 5 million residents – just before the city enters the frigid winter season.

“Transactions have slowed down in recent weeks following a strong rebound in June/July.

“We are not particularly worried about the recent slowdown in sales in the city, as we continue to see strong end-user demand both within the city and from the surrounding smaller cities, given the ongoing improvement in living conditions (better transportation links and infrastructure) and a relatively low price among tier-2 cities,” Deutsche said.

Residential: Stable

Home prices have little changed despite a dip in volume, Deutsche said.

“In Shenyang, sales have slowed down as we approach the traditional low season in the Northern provinces (December to February) and developers slow down on project launches. Buyers are generally adopting a wait-and-see attitude as the government reiterates its stance of avoiding an overheating property market.”

However, the research note added that prices are “mostly stable,” with only some cuts in smaller projects developed by smaller players.

“Buyers are looking for more clarity ahead and developers are slowing down as sales targets are well assured for this year and the low season is approaching.”

Office/Retail: Longer-term Concerns Remain

While Shenyang has no new Grade A supply entering the market in 3Q12, longer-term (2H12-2014) supply concerns remain.

“Based on our meeting with DTZ, Shenyang will see a significant increase in Grade A office supply starting 2013, with estimated future supply exceeding the city’s current total stock by more than 150%.

“As one developer said during our visit, ‘there are a number of complex development projects with GFA of 200k-400ksqm in the pipeline, leading to longer-term concerns over the commercial market of the city’.”

For growth, Deutsche said its top picks are COLI, CR Land, COGO and Sunac.

“For value, we recommend developers with accelerating sales in 4Q: Country Garden, R&F and KWG.”

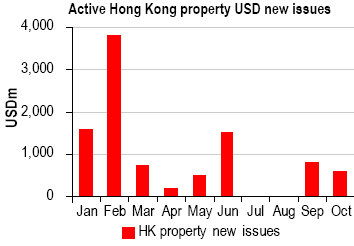

HSBC: Strong Property Bond Activity

Hong Kong property companies, including landlords and developers, have raised a record USD9.7bn from the USD bond market YTD, HSBC said.

“Despite massive 200bp spread tightening from primary issuance levels, BBB Hong Kong property credits still offer good relative value,” the research note said.

Hence, it is raising trading calls on Henderson’s HENLND’17, Kerry’s KERPRO’17, New World’s NWDEVL’20 to Buy from Hold; The Wharf’s WHARF’17N, Wheelock’s WHEELK’17 to Hold from Sell; reiterate Buy Nan Fung’s NANFUN’17, ’22.

Hong Kong property companies have been active in US dollar bond issuance YTD, with a number of debut names tapping the US dollar bond market for funding.

“A good example is Nan Fung, an unlisted Hong Kong developer, which tapped the USD bond market three times and raised 900 million usd via issuances of 5- and 10-year bonds,” HSBC said.

It added that with “signs of liquidity easing” in the syndicated loan market of late, it believes property companies that have already tapped the dollar bond market for funding will shy away from primary issuance in 4Q12.

“That said, new issuance in 4Q should shift to second-tier players in the Hong Kong property space. Credit selection is important, in our view, given the much smaller business scale and lack of sizeable recurrent cash flow for this group of credits.”

Sixteen Hong Kong property issuers have raised a record USD9.7bn, up 11-fold from the USD800m raised in full-year 2011, and accounting for almost one-tenth of the ytd Asia ex- Japan and Australia G3 bond issuance of USD101bn.

“Selective Hong Kong property companies are more active in pursuing China expansion, including The Wharf, Kerry Properties, Hang Lung and New World. Specifically, The Wharf has set a medium-term target of having 50% of its asset base in China versus 37% (33% in properties) as of June 2012; while Hang Lung has been disposing of non-core investment properties as well as residential units in Hong Kong and redeploying the capital into China investment property projects.”

Macquarie: China Property

Macquarie Equities Research said that ecently, there have been more objections to the property tax proposals in the PRC mass media.

Currently, Chongqing levies the property tax on both existing and new purchased luxury housing, with rates ranging between 0.5 and 1.2% for different properties.

“In comparison, Shanghai only charges new purchased homes with an effective tax rate of 0.28-0.42%,” Macquarie said.

The research house added that it believes there will be no major policy changes for the next nine months (i.e., no lifting of the home purchase restriction or extensive property tax implementation).

“In terms of stock picking, company-specific analysis is more important than policy analysis or macro predictions.

We expect Shimao Property (813 HK, HK$13.10, Outperform, TP: HK$15.36), Sunac China (1918 HK, HK$3.85, Outperform, TP: HK$4.92) and China Resources Land (1109 HK, HK$16.52, Outperform, TP: HK$21.53) to outperform peers due to their flexible pricing, strong execution skills and improving strategies to adapt to the market.”

Bocom: Hong Kong Property

Bocom International said the property prices in Hong Kong have risen 16.5% YTD and are 8% higher than the 1997 peak.

“However, we believe this also reflects the overall inflationary pressure, including the 11% increase in income base.

“At the same time, purchasing power is still far from drying up, with the overall affordability ratio low at 9.2% and skewing towards the low end of the 20-year range,” Bocom said.

The research house added that the government’s primary responsibility is to ensure sufficient accommodation.

“Therefore, we expect further room for mortgage tightening, if necessary.

“Nevertheless, genuine purchasing power should continue to support the market, and we expect a mild 5% increase in property prices in 2013E.”

And given the asymmetric leverage between buyers and sellers in the secondary market, Bocom expects further flow of purchasing power into the primary market, which continues to favor developers with strong sales pipelines.

“Our top picks are SHKP (16 HK) and Wheelock (20 HK). On the other hand, we downgrade Sino Land (83 HK) to SELL given its short HK landbank and high valuation.

“We maintain an ‘Outperform’ on the sector.”

See also:

Top ChiNext Disasters

CHINEXT BOARD: PRC's Tycoon Factory

CHANGING FACES: Five Sectors Turning Bullish

China Shares No Compass For Economy