Excerpts from latest analyst reports……

CIMB says BRIGHT WORLD’S fair value is 67.5-91 cents

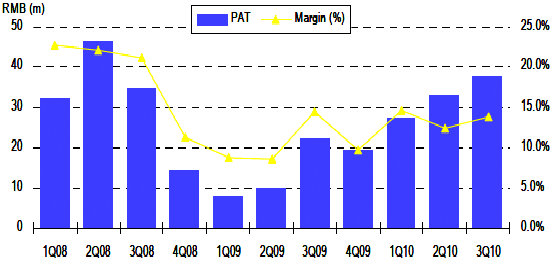

We visited Bright World’s manufacturing facilities in China last week and walked away feeling positive on its near-term outlook.

We sense that Bright World’s recovery had been intact in the December quarter, and believe the momentum could flow into 2011 as it focuses on improving its product mix, to drive up margins.

Assuming it can repeat its 3Q10 performance in 4Q10, full-year net profit should be Rmb130m-140m, almost going back to its peak earnings in FY07 before the financial crisis. This would translate into 8-9x CY10 P/E on more than a 100% yoy jump in EPS.

Management hopes to achieve 30% earnings growth in 2011, which would bring down P/Es to 6-7x if successful. Bright World trades below book value at 0.7x.

There are no direct comparables in Singapore, but we refer to the valuations of SGX-listed semiconductor equipment contract manufacturer, UMS (UMSH SP, BUY), Hong Kong-listed plastic injection equipment maker, Chen Hsong Holdings (57 HK, NR), and Japan-listed competitor, Aida (6118 JP, NR).

By P/E, Aida trades at 23.7x CY11 consensus forecast, Chen Hsong at 10.6x and UMS at 7.1x. By P/BV, they trade at 0.6x, 1.0x, and 1.0x, respectively.

We believe 8-10x forward P/Es for equipment makers like Bright World are reasonable, implying a fair value of S$0.675 to S$0.91 for Bright World.

Recent story: SITE VISIT: BRIGHT WORLD Stamping Major Name For Itself In PRC

Lim & Tan Securities maintains 'buy' call on SINO GRANDNESS

We visited a couple of Chinese supermarkets (Ren Ren Le, Xin Yi Jia, Vanguard, Wan Tian Tong, Shi Ji Hua Lian) in Guangzhou which started to carry Sino Grandness’ “Xian Lu Yuan” mixed fruit and vegetable juices late last year.

* We were surprised that despite having only been introduced recently, they were already sharing the same shelf space as big players such as Coca Cola’s “Minute Maid”, China Hui Yuan Juice (which Coca Cola had wanted to buy in 2008 for US$2.4bln but was stopped by the Chinese government), Kang Si Fu and Bei Qi.

* The stock had recently significantly (from the 45 cents level to 56.5 cents before pulling back to 51.5 cents currently) since Jan 7’11 when we first highlighted the stronger than expected response to their new juice business.

* We believe the company is at the early stage of growth and its forward PE of 5x remains undemanding relative to growth of 25-30%.

The company is also a good potential dual listing candidate given that its peers (in Hong Kong and Taiwan) are trading at much higher multiples of 30+x PE notwithstanding the fact that they are much more established and bigger in size.

* We maintain our BUY recommendation.

Recent story: DMG raises SINO GRANDNESS target price from 56 c to 68 c

SIAS Research sets $1.05 value for UMS

Analyst: Liu Jinshu

UMS has a well articulated and convincing strategy that we believe sets it apart from its peers. Accordingly, we see further share price upside potential for UMS. Maintain Increase Exposure call based on an upgraded intrinsic value of S$1.05

Bumper dividend payout: UMS’s directors have proposed a dividend of 3 S cents per share for 4Q FY10. This brings total dividends for FY10 to 5 S cents per share, translating to a yield of about 8.5% (based on previous close of S$0.590). We note that UMS’s cash generating ability remains strong, with net cash from operating activities coming in at 1.45x of net profit. As such, we can continue to expect a high dividend payout going forward.

Recent story: UMS: "Momentum is still strong, good for 3 more quarters...."