Executive Chairman Zhou Jun. Photo by Sim Kih

Executive Chairman Zhou Jun. Photo by Sim Kih

THE EARNINGS of SIIC Environment Holdings may have multiplied by over 10 times over the past 5 years and its market cap by close to 20 times, but its growth story is far from over.

“We intend to continue with our M&A strategy, targeting an increase in annual capacity for waste water treatment of one to two million tons," said Executive Chairman Zhou Jun at a media briefing last Friday.

About 80% of its revenue comes from wastewater treatment but last month, it forayed into the next hot sector in environmental protection - sludge treatment.

SIIC Environment and International Finance Corp eachinvested US$4 millionin a leading PRC sludge treatment player, MTI Environment.

(International Finance Corp is a venture development arm of World Bank specializing in third world nation investments.)

“MTI is one of the top 3 EPC sludge treatment players in PRC. This sector has enormous potential in China,” said Mr Zhou.

“Sludge treatment requires higher technical know-how compared to waste water treatment. Investing in MTI will give us access to this know-how.

“We can collaborate with MTI to embark on BOT sludge treatment projects.”

In the cards is also the potential spin-off of its sludge treatment business for a Hong Kong IPO. It also plans to dual-list the Singapore listed entity on the Hong Kong Stock Exchange.

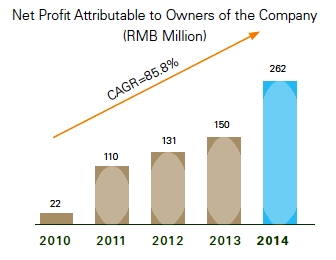

The Group's net profit attributable the shareholders increased from Rmb 22 million in FY2010 to Rmb 262 million in FY2014.

The Group's net profit attributable the shareholders increased from Rmb 22 million in FY2010 to Rmb 262 million in FY2014.

(International Finance Corp is a venture development arm of World Bank specializing in third world nation investments.)

“MTI is one of the top 3 EPC sludge treatment players in PRC. This sector has enormous potential in China,” said Mr Zhou.

“Sludge treatment requires higher technical know-how compared to waste water treatment. Investing in MTI will give us access to this know-how.

“We can collaborate with MTI to embark on BOT sludge treatment projects.”

In the cards is also the potential spin-off of its sludge treatment business for a Hong Kong IPO. It also plans to dual-list the existing Singapore listed entity (SIIC Environment) on the Hong Kong Stock Exchange.

Mega deal to acquire a prominent PRC wastewater treatment player

SIIC Environment Executive Chairman Zhou Jun speaking with the media at Conrad Centennial Hotel last Friday. Photo by Ala ZhangIn March, SIIC Environment inked a deal to acquire 100% in Fudan Water Engineering and Technology for Rmb 1.1 billion (S$240.5 million) from Global Environment Investment.

SIIC Environment Executive Chairman Zhou Jun speaking with the media at Conrad Centennial Hotel last Friday. Photo by Ala ZhangIn March, SIIC Environment inked a deal to acquire 100% in Fudan Water Engineering and Technology for Rmb 1.1 billion (S$240.5 million) from Global Environment Investment.

The deal includes SIIC Environment taking over Fudan Water's debt of Rmb 479.18 million (S$107.8 million), meaning that its total purchase consideration amounts to Rmb 1.548 billion (about S$348.3 million).

Fudan Water Group has 10 projects in Shanghai, Jiangsu, Zhejiang and Guangdong.

Based on Fudan Water's treatment capacity of over one million tons a day, the purchase consideration translates into a ballpark price of less than Rmb 1,548 per ton of daily treatment capacity.

With the completion of the merger with Fudan Water Group, its total capacity will increase to 6.4 million tons a year.

Fudan Water Group is estimated to add over Rmb 80 million to the Group’s bottom line.

Assuming that SIIC Environment's share price holds up after the issue of 1.56 billion shares for its acquisition of Fudan Water, its market cap would be around S$2.4 billion. When Mr Zhou first joined the board in April 2010 (when it was known as Asia Water Technology prior to the RTO by Shanghai Industrial Investment Corp), its market cap was only between S$100 million and S$150 million. Bloomberg data

Assuming that SIIC Environment's share price holds up after the issue of 1.56 billion shares for its acquisition of Fudan Water, its market cap would be around S$2.4 billion. When Mr Zhou first joined the board in April 2010 (when it was known as Asia Water Technology prior to the RTO by Shanghai Industrial Investment Corp), its market cap was only between S$100 million and S$150 million. Bloomberg data

On 13 May, SIIC Environment posted 1QFY2015 net profit growth of 1.1% to Rmb 84.2 million, after a posting CAGR of 85.8% over the past 5 years.

1QFY2015 net profit attributable to shareholders was up 7.5% at Rmb 68.4 million.

On 14 May, Maybank Kim Eng analyst Wei Bin maintained his ‘Buy’ call on SIIC Environment, citing strong M&A momentum ahead of its Hong Kong dual-listing plan.

The analyst raised his target price to 26 cents (30x P/E), in line with Hong Kong listed peers.