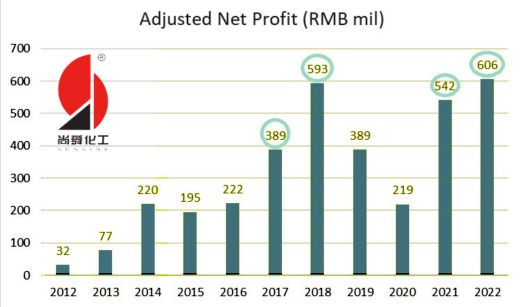

| • It's been 16 years since China Sunsine listed on the Singapore Exchange in July 2007. That longevity points to it being a strong and real made-in-China business, at least compared to the many S-chips that have fallen by the wayside. • And China Sunsine has been consistently profitable over a long period, and has reinvested some profits to build up its production capacity to capture market share.  Strong but choppy profit uptrend. Strong but choppy profit uptrend. Profit adjusted for tax credit due in 2017 but included in 2018 financial statement, and for tax credit received in 2022 for overpayment in 2021. Profit adjusted for tax credit due in 2017 but included in 2018 financial statement, and for tax credit received in 2022 for overpayment in 2021. • Its business is global -- serving more than two thirds of the top 75 tyre makers in the word, including Bridgestone, Michelin, Goodyear, and Pirelli.

• With a market cap of around S$370 million, the stock is trading at ~5X PE (CGS-CIMB forecast) with a 3.9% dividend yield -- and a PE ex-cash of 1.5x. That is not an unattractive valuation. Read more of what CIMB analysts have to say below.... |

||||||||||

Excerpts from CGS-CIMB report

Analysts: Ong Khang Chuen, CFA & Kenneth Tan

China Sunsine Chemical Holdings -- Market competition remains intense

■ We deem Sunsine’s 2Q23 net profit of Rmb128m (+90% qoq, -53% yoy) as a low-quality beat, with outperformance driven by non-operational items.

■ Reiterate Hold with a lower TP of S$0.42. |

||||

| 1H23: outperformance driven by non-operational items |

China Sunsine’s 2Q23 net profit of Rmb128m (+90% qoq, -53% yoy) brought 1H23 net profit (-54% yoy) to 59% of our FY23F forecast.

We deem this as a low-quality beat, given that the outperformance was mainly driven by non-operational items (FX gains, interest income).

2Q23 sales volumes rose 4% qoq and 5% yoy, with its more flexible pricing strategy; however, revenue was flattish qoq as ASP eased on the back of

| 1) intensified market competition, and 2) a decline in raw material costs. |

2Q23 GPM improved by 2.8% pts qoq to 25.2% but was weaker vs. the high base last year (2Q22: 34.6%).

| Cautious outlook amid intense competitive pressure |

According to sci99.com, a Chinese commodity market information service provider, rubber accelerator prices rebounded slightly in Aug.

Sunsine attributed the higher prices mainly to rising input costs. Management has not observed significant improvements in downstream demand YTD and thinks competitive pressure could ramp up further with likely incoming industry supply by end-2023F.

| "Management has not observed significant improvements in downstream demand YTD and thinks competitive pressure could ramp up further with likely incoming industry supply by end-2023F." |

While Sunsine is optimistic of achieving further sales volume growth, we think its profit spread (on a per tonne basis) could remain under pressure with the adoption of its “flexible pricing strategy” amid intense market competition.

Given China’s recent economic woes, we maintain our cautious stance on expectations for a demand recovery until we see more government policies rolled out to promote a more sustained recovery in consumption.

The Chinese government’s recent announcement on ramping up policy support for the domestic automobile sector is a good start, in our view.

|

Full report here