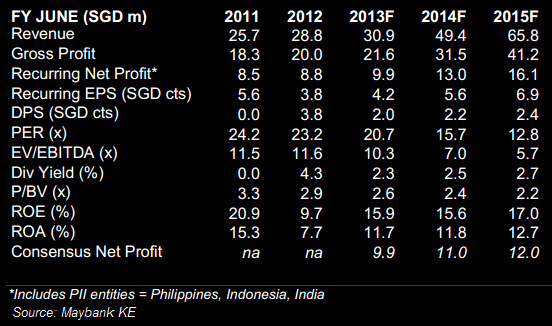

Excerpts from analysts' reports

Maybank Kim Eng initiates coverage of Cordlife with $1.29 target

Maybank Kim Eng initiates coverage of Cordlife with $1.29 target

Analyst: John Cheong

Jeremy Yee, CEO of Cordlife. Photo by Sim KihWe initiate coverage on cord blood bank Cordlife with a BUY rating and a Street-high TP of SGD1.29, which offers 47% upside.

Jeremy Yee, CEO of Cordlife. Photo by Sim KihWe initiate coverage on cord blood bank Cordlife with a BUY rating and a Street-high TP of SGD1.29, which offers 47% upside.

With a strong platform to expand its product range combined with dominant positions in Singapore, Philippines, Indonesia and a strong presence in Hong Kong, India and China, it is poised to transform into Asia’s infant and maternal healthcare products champion over the next two years, riding the sweet side of both developed and emerging markets.

Jeremy Yee, CEO of Cordlife. Photo by Sim KihWe initiate coverage on cord blood bank Cordlife with a BUY rating and a Street-high TP of SGD1.29, which offers 47% upside. With a strong platform to expand its product range combined with dominant positions in Singapore, Philippines, Indonesia and a strong presence in Hong Kong, India and China, it is poised to transform into Asia’s infant and maternal healthcare products champion over the next two years, riding the sweet side of both developed and emerging markets.

With the completion of recent acquisitions of Philippines, Indonesia and India’s operation last week, Cordlife has built a far-reaching platform.

Next, we expect it to launch a wider range of maternal and infant healthcare products to better utilise its regional platform, which will drive economies of scale, margins and both top and bottomline growth.

Already, it has expanded from just cord blood to include umbilical cords. However, the sky’s the limit and there is great potential to add more products and services that could be immediately earnings accretive.

Next, we expect it to launch a wider range of maternal and infant healthcare products to better utilise its regional platform, which will drive economies of scale, margins and both top and bottomline growth.

Already, it has expanded from just cord blood to include umbilical cords. However, the sky’s the limit and there is great potential to add more products and services that could be immediately earnings accretive.

At current prices, we believe the market has not fully priced in Cordlife’s favourable market position, strong regional presence, excellent product expansion opportunities, exceptional margins, high competitive advantages and sustainable earnings.

As a result, its valuations are still deeply depressed. Our TP of SGD1.29 is pegged at 23x FY14F PER, which is in line with its global peers.

As a result, its valuations are still deeply depressed. Our TP of SGD1.29 is pegged at 23x FY14F PER, which is in line with its global peers.

Nomura reiterates $1.80 target for Biosensors

Analysts: Jit Soon Lim, CFA, & Wen Jie Chan

Biosensor's Axxess stent in a blood vessel. Illustration from companyWe lower our earnings for FY14F and FY15F by 6% to reflect the higher costs the group will likely incur as it expands its product base and supports its newly acquired medical imaging business.

Biosensor's Axxess stent in a blood vessel. Illustration from companyWe lower our earnings for FY14F and FY15F by 6% to reflect the higher costs the group will likely incur as it expands its product base and supports its newly acquired medical imaging business.

The higher costs, in our view, will be mitigated by stronger revenue growth from new product launches. We forecast EPS growth of 8% this year before accelerating to 15% CAGR over the following two years.

We reiterate our Buy rating with a price target of SGD1.80.

Recent story: Buy BIOSENSORS, Sell GOLDEN AGRI, AUSGROUP

Analysts: Jit Soon Lim, CFA, & Wen Jie Chan

Biosensor's Axxess stent in a blood vessel. Illustration from companyWe lower our earnings for FY14F and FY15F by 6% to reflect the higher costs the group will likely incur as it expands its product base and supports its newly acquired medical imaging business. The higher costs, in our view, will be mitigated by stronger revenue growth from new product launches. We forecast EPS growth of 8% this year before accelerating to 15% CAGR over the following two years.

We reiterate our Buy rating with a price target of SGD1.80.

Shares oversold following “disappointing” 4Q results. Biosensors has pulled back by 9% post the 4Q results at the end of May.

Valuations are attractive, in our view, at 12x FY14 EPS, underpinned by our sum-of-the-parts valuation of SGD1.80 per share and net cash of USD337mn (SGD0.25 per share).

In addition, the group will pay a dividend of USD0.02/share by early August 2013.

In addition, the group will pay a dividend of USD0.02/share by early August 2013.

Recent story: Buy BIOSENSORS, Sell GOLDEN AGRI, AUSGROUP