JP Morgan: XTEP Enjoys Largest Net Asset Backing

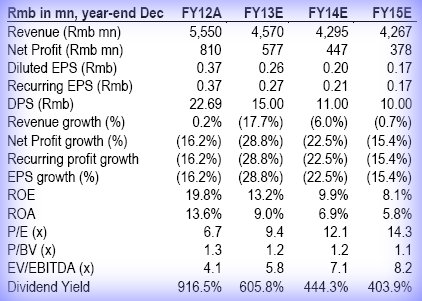

JP Morgan said fashion sportswear play Xtep International Holdings Ltd (HK: 1368) enjoys the largest net asset backing among its rivals.

“That means Xtep is trading at the lowest price/franchise value in the sector,” JP Morgan said.

Xtep is China's top fashion sportswear play. Photo: XtepThe research house is assuming coverage of Xtep with an “Underweight” call and a target price of 2.4 hkd (recent share price 3.1).

Xtep is China's top fashion sportswear play. Photo: XtepThe research house is assuming coverage of Xtep with an “Underweight” call and a target price of 2.4 hkd (recent share price 3.1).

Xtep’s estimated tangible net asset value is approximately 1.5-2.0 hkd per share.

JP Morgan estimates tangible net asset value by disregarding value associated with the brand and distribution network and attributing value only to: (1) Xtep's net cash position; and (2) the value of the company's plant as if it was to be used as an OEM plant.

Channel inventory issue likely to take some time

Inventory issues associated with the China sportswear industry date back pre-2008.

From 2009 to 2011, combined sales of Chinese sportswear companies increased significantly more than the China sales of international sportswear entrants (Adidas and Nike).

JP Morgan said that if it were to assume that sales for the top seven domestic Chinese sportswear brands should have only grown at rates similar to Adidas in Greater China, then excess inventory sold into the channel by the top seven domestic brands would have amounted to ~39 billion yuan for the three years to Dec-11.

Source: JP Morgan

Source: JP Morgan

And if the research house were to assume that sales for the top seven domestic Chinese sportswear brands should have only grown at rates similar to Nike in Greater China, then excess inventory sold into the channel by the top seven domestic brands would have amounted to ~14 billion yuan for the three years to Dec-2011.

“Our FY2014 earnings forecasts for Xtep are ~35% below consensus. We believe there is risk of EBIT margin compression over the longer term, such that margins contract to be in line with international peers,” JP Morgan added.

It forecasts Xtep’s longer-term EBIT margins will reduce to the low teens compared to ~20% in FY2012.

Photo: BelleBocom: BELLE’S Sportswear Push Slower than Expected

Photo: BelleBocom: BELLE’S Sportswear Push Slower than Expected

Bocom International said the expansion into the sportswear sector by Belle (HK: 1880) has been underwhelming.

“For sportswear, 54 stores were opened in 1Q13, at 11% of our full-year estimate of 500 stores and below our expectation,” Bocom said.

Belle’s latest release of 1Q13 SSS growth (4.5% for footwear and 11% for sportswear) seems in line with market expectation (vs. Bocom’s full-year forecast of +5%).

The research house urged investors not to read into things too positively, given the particularly low base in the first quarter last year (footwear +2.8%; sportswear -2.4%) and the bigger sales discount offered this year.

Belle recently 13.2 hkd“Furthermore, our concerns about the group’s margin pressure remain, amid sustained heavy promotional activities and high new store losses due to cannibalization resulting from its aggressive expansion.”

Belle recently 13.2 hkd“Furthermore, our concerns about the group’s margin pressure remain, amid sustained heavy promotional activities and high new store losses due to cannibalization resulting from its aggressive expansion.”

Bocom is reiterating its “Neutral” call on Belle and target price of 12.5 hkd (based on 18.2x FY13E PE, continuing at a 10% premium to key consumer peers).

See also:

HK-listed Sportswear Plays: Big Dividends, Small Profits?