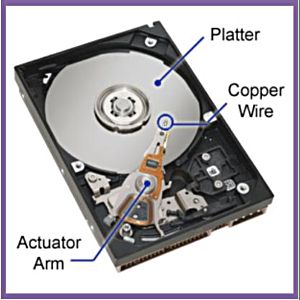

Listed on the mainboard of SGX since 1994, the company is one of the leaders in the manufacture of precision components and assemblies. It is a key provider of actuator arms, assemblies and other related parts for the global hard disk drive (HDD) industry. Headquartered in Singapore, the company has 4 manufacturing facilities in China and Thailand and employs around 3,5000 people.

Highest profit in 5 years. FY2021 net profit rose 8% YoY to S$15mn as revenue increased 18% YoY to S$471mn. Core net profit would have been higher at S$18mn if not for a S$2.4mn charge for impairment of goodwill.

The company has proposed a final dividend of 0.5 Sing cents and a special dividend of 0.5 Sing cents, which, together with the interim dividend of 0.5 Sing cents, brings the total dividend for FY2021 to 1.5 Sing cents.

Outlook and diversification. BWAY remains cautiously optimistic on the HDD business as it expects near-term demand to remain strong. Trendfocus, in a 2 Feb 2022 report, projected a 11.4% CAGR in total HDD revenue for the period 2021 to 2026.

In terms of diversification, BWAY acquired a 55% stake in China-based Beijing Ant Brothers Technology in 2022 to establish a Robotics Business unit. The group has commenced marketing activities for its robots in Singapore ,Thailand and the Philippines and expects revenue contribution.

Attractive valuations. BWAY currently trades at only 5.2x core FY2021 P/E (excluding non-recurring losses), or 6.7x FY2021 P/E (headline EPS) a significant discount to SG-listed technology manufacturing peers.