Kingsley Lucas Lim (photo) contributed this article to NextInsight. He had originally published it on his site, The Holy Financier.

Kingsley Lucas Lim (photo) contributed this article to NextInsight. He had originally published it on his site, The Holy Financier.

| In today’s tale of two companies, namely Hanwell Holdings and Tat Seng Packaging, we attempt to go beyond the numbers of these 2 extremely relatable companies and propose why holding companies may be excellent control structures but poor vehicles for the creation of shareholder value for minority shareholders like us. Hanwell Holdings is a holding company that has varied businesses such as providing healthcare solutions, fast moving consumers goods and that of franchise provision shops. Notably, Hanwell Holdings owns approximately 64% of Tat Seng Packaging Group Ltd, a manufacturer of corrugated paper and packaging. Hanwell considers Tat Seng Packaging Group to be a strategic investment. |

Background Of Hanwell Holdings & Tat Seng Packaging

Tat Seng Packaging has a market capitalisation of $96 million with extremely conservative debt levels of 1.42 times Debt-EBITDA. Enterprise Value-Ebitda for Tat Seng Packaging is 2.8.

The latest reported revenue for Tat Seng Packaging is $333.3 million of revenue. Comparatively, Hanwell Holdings has about $500 million of revenue and trades at an EV-EBITDA of 3.46.

You would be tempted to think that Hanwell Holdings should trade at a higher market capitalisation than Tat Seng Packaging considering the reported sales revenue.

You are right but what will astound you is the very small difference in market capitalisations despite a huge portion of the revenues obtained from Tat Seng Packaging, the operating subsidiary of Hanwell Holdings. At the time of this writing, Hanwell Holdings trades at a market capitalisation of just $143 million.

|

Company |

Market Capitalisation |

Revenue |

|

Hanwell Holdings |

$143 m |

$501 m |

|

Tat Seng Packaging |

$96 m |

$333 m |

And it gets more interesting.

Tat Seng Packaging has grown by leaps and bounds, not organically but through acquisitions.

While the growth by acquisition strategy usually results in huge write downs and impairments during dire business conditions, Tat Seng Packaging or rather the management of Tat Seng, headed by Dr Allan Yap had done fairly well not to overpay for acquisitions in my opinion.

So over the years, the company had grown from $34.8 in revenue in FY 2004 million to $333.3 million in revenue in FY 2018, a factor of close to 10 times.

Hanwell Holdings Acquires Tat Seng Packaging

In 2005, Hanwell Holdings, headed by Allan Yap, acquired Tat Seng Packaging and management marked a milestone in its history by proclaiming “The business is now in an excellent position to face the increasingly challenging business environment and benefit from our efforts to further strengthen our value chain. We can now seek out more profitable businesses which can synergise with our existing infrastructure”.

Hanwell Holdings paid an effective $13.8 million for $29.4 million worth of net assets of Tat Seng Packaging, resulting in a negative goodwill of $7.9 million in 2005. Then, Tat Seng’s EBITDA for the year ending June 2005 was $5.6 million and the net income was $2.5 million earned on a total shareholders’ equity of $39.6 million. Tat Seng paid $1.2 million and $3.8 million in dividends in 2004 and 2005.

On some back of the envelope calculation, if we value the dividend stream as a perpetuity paying 5% per annum, the average of a $2 million dividend stream would be worth some $40 million. 64% of that is equal $25.6 million, bearing in mind that Hanwell Holdings, then PSC Corporation, paid an effective price of $13.8 million for that dividend stream.

Retained earnings by Tat Seng was compounded at a return on equity of between of between 6% and 8% from FY 2004 to FY 2006, which implied that shareholder’s equity could compound at between 6% and 8% over the next few years and perhaps into the future.

Reading the annual reports, I get a sense of what Dr Allan Yap was trying to do. He knew that the corrugated board and packaging industry was fragmented. With Singapore’s growth stifled somewhat around economic and other constraints, it made sense to look overseas for growth opportunities. And one of the best countries to operate such low margin businesses was in China.

The country had slower growth over the last decade but it was by far one of the fastest growing countries in the world. Dr Allan Yap was calculative. He made sure to extract that growth from economic zones in China that was abuzz with industry and commerce.

The entire packaging industry was somewhat fragmented and had too many players. But a consolidation at the right prices seemed a decent strategy especially if you pursue growth at the right prices. As far as I can tell, Tat Seng Packaging paid for assets that was mostly profitable and did not pay too high a price for these assets. For more on its acquisitions, you can find some of them below.

Hanwell Holdings Uses Tat Seng As An Acquisition Vehicle

|

• 2008 – Tat Seng Packaging Acquired United Packaging

|

However all was not smooth as with all low margin businesses. Competition heated up in China and together with higher raw material prices, operating margins dipped to 4.34% from 6.04% in FY 2010. Gross margin was 15.36% in FY 2011 as compared to 17.45% the year earlier.

The rationale then was to ramp up production facilities via acquisitions and then ramp up sales through its sales force, which eventually materialised over the years.

Double Digit Return On Equity For Tat Seng Packaging

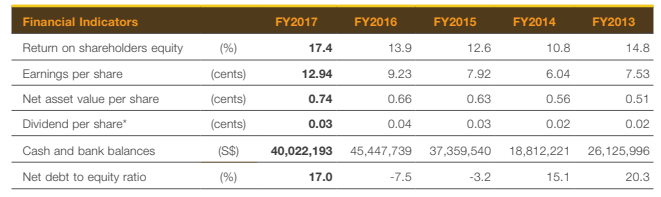

In the results of Tat Seng Packaging over the last several years, it seems that the acquisition of Tat Seng Packaging by Hanwell Holdings has panned out quite well. Tat Seng enjoys a double digit return on equity and FY 2017’s results were phenomenal for a packaging company, proving that low return businesses can have good outcomes at the right prices.

Hanwell Holdings Vs Tat Seng Packaging – Different Agendas

Hanwell Holdings is a company with a different agenda as compared to Tat Seng Packaging. It was set up as a holding company. Formerly called Provisions Suppliers Corporation Ltd, the company was founded as a provisions supplier and built its business by acquiring distribution rights to fast moving consumer goods.

Over time, the company had become a major player in the distribution scene and it even set up Econ Minimart, a franchise retail chain of provisions and other supplies. In 2000, the Hanwell Holdings held interests in diverse business segments such as healthcare, hotel and leisure. It even owned a golf course and country club in Malaysia.

With its diverse business interests, it was clear at the outset that Hanwell Holdings was set up to hold several entities, a holding company. Then in 2002, Hanny Holdings, headed by Allan Yap became the group’s major shareholder.

Essentially, Allan Yap purchased control of Hanwell Holdings and eventually used Hanwell as a vehicle to purchase stakes in other businesses. Eventually, as we know it, Hanwell Holdings purchased a majority stake in Tat Seng Packaging Group. This is typical of a holding company structure.

In 2004 itself, Hanwell Holdings had $141.1 million in revenue and had a market capitalisation of $141.9 million. By 2018, the group now has more than tripled its revenue to $501.6 million but it only has $143 million in market capitalisation.

The question is why has the market not recognised the group’s growth in revenues?

Firstly, dividends paid out had always been paltry to say the least. In 2004, the group paid out $3.6 million in dividends while for its latest fiscal year, the group only paid up $5.1 million in dividends despite revenue more than tripling over the same period.

Comparison Of Cumulative Dividends Paid

|

Company |

2004 to 2018 Cumulative Dividends Paid |

2014 to 2018 Cumulative Dividends Paid |

|

Tat Seng Packaging |

$37.8 m |

$21.9 m |

|

Hanwell Holdings |

$34.6 m |

$10.1 m |

Comparison Of Growth Of Tangible Book Values Per Share

|

Company |

2004 Tangible Book/share |

2018 Tangible Book/share |

|

Tat Seng Packaging |

0.26 |

0.81 |

|

Hanwell Holdings |

0.49 |

0.51 |

While holding companies make very good control vehicles, they are extremely inefficient corporate structures from the standpoint of a minority shareholder.

The holding company thus serves its purpose as a controller of its subsidiaries but in so doing, puts too many layers between the operating assets and the shareholders.

Think of it this way. If a subsidiary of a holding company is laden with debt, there is a high chance of the subsidiary going under and falling into bankruptcy.

When that happens, the holding company is typically insulated from liability from a legal standpoint. This is the advantage of a holding company.

However, that is also a disadvantage because these corporate layers insulate the holding company shareholders from the subsidiary’s cash flows at the operating level.

Tat Seng Packaging is the operating entity in this case. By comparison, from 2014 to 2018, Tat Seng Packaging has paid $21.9 million in dividends but Hanwell has only paid some $10.1 million.

That is a huge discrepancy in my opinion, considering that Hanwell received approximately $14 million of those dividends paid by Tat Seng.

Heck! Apparently, those dividends did not adequately flow from Tat Seng to Hanwell’s shareholders.

Considering that vantage point, it makes sense to invest in the operating subsidiary instead of the holding company in many instances.

Of course, there are always exceptions to this. Berkshire Hathaway is one. However, I believe Berkshire Hathaway is an anomaly driven largely by Warren Buffett’s personality.

| Conclusion At 26 cents per share, Hanwell Holdings trades at slightly above its net current asset value per share of 23 cents per share and at a discount of 49% to the tangible book value. For Hanwell to trade significantly above these prices and closer to the tangible book value per share, Hanwell has to return more of its excess capital to shareholders. But I am not sure if that is going to happen anytime soon for Hanwell is used as a holding company whose excess cash is typically utilised towards making new strategic investments. Alas, the charts of both companies paints a clear message, if at least historically.   Charts : Google Finance Charts : Google Finance |