ST ENGINEERING -- target $4.30; QT VASCULAR -- 51 cents

Details

Excerpts from analysts' reports

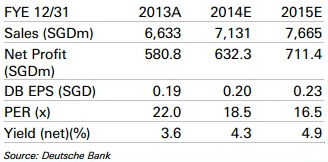

Deutsche Bank has 'buy' call on ST Engineering and S$4.30 target

Analyst: Kevin Chong

Stability and diversification

At the investor meetings (at dbAccess Asia Conference 2014), STE highlighted how its diversified operations in defence, government and commercial markets have provided stability for the group over the years.

Its exposure to the four divisions in Aerospace, Electronics, Land Systems and Electronics has also contributed to its operational resilience. STE’s balance sheet remains robust and it is still triple-A rated by Moody’s and S&P.

Its FY13 net profit split was as follows: Aerospace 45%, marine 19%, Land Systems, 16%, and Electronics 23%.

Order book and dividend policy

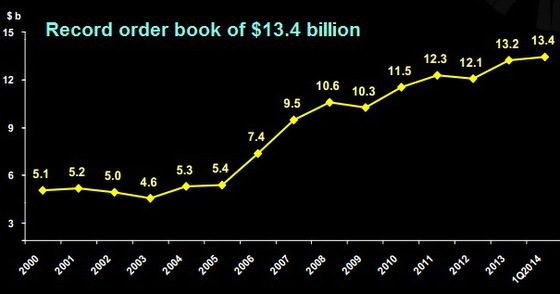

STE’s order book as at 1Q14 stood at a record S$13.4bn, and has more than doubled since 2005, providing healthy visibility for the group.

Management has maintained its guidance for higher revenues and PBT in FY14 vs. FY13, and indicated that 1H14 would be comparable yoy, which implies a stronger 2H14.

On dividends, STE highlighted that its FY13 dividend payout at 80% is healthy and that the reduction from 90% previously was largely to reduce the impact from withholding taxes when funds are repatriated out of the US.

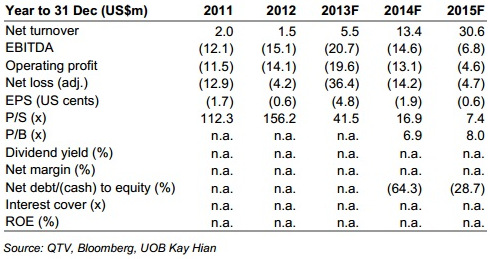

UOB Kay Hian initiates coverage of QT Vascular with 51-c target

Analyst: Andreas Isabel Co, CFA

QT Vascular (QTV) is engaged in the design, assembly and distribution of advanced therapeutic solutions for the minimally-invasive treatment of complex vascular diseases.

Its product portfolio includes two coronary devices and three peripheral devices, one of which is its flagship Chocolate® PTA Balloon Catheter (Chocolate PTA).

It carries out its operations from two locations – Pleasanton, California and Singapore – and has a distribution presence in the US, Europe, Japan and China.

INVESTMENT HIGHLIGHTS

• Initiate coverage with a BUY; target price of S$0.51 represents 36% upside.

Our target price was derived using a 2015F P/S ratio of 10x, which is based on completed comparable medical device M&A deals beginning 2012.

The multiple is at the high end of the range, justified by QTV’s revenue-generating product portfolio, strong distribution partnerships and potentially paradigm-changing device in the Drug-coated Chocolate PTA (DCC).

We also note that a loss-making US medical device company, TriVascular Technologies, was listed on the NASDAQ in Apr 14 at an implied 14x 2013 P/S.

At 14x, our target price for QTV would be S$0.71 but this is not our base case scenario.

At the investor meetings (at dbAccess Asia Conference 2014), STE highlighted how its diversified operations in defence, government and commercial markets have provided stability for the group over the years.

At the investor meetings (at dbAccess Asia Conference 2014), STE highlighted how its diversified operations in defence, government and commercial markets have provided stability for the group over the years.