DBS Vickers initiates ‘Buy’ call on Consciencefood (23.5c) with 38-ct target price

Manufacturer and seller of instant noodles and snack noodles. Conscience Food (CSF) is engaged in the manufacturing and sale of instant noodles and snack noodles in Indonesia with an estimated market share of 4%. CSF’s products are sold across six major provinces in Sumatra (North Sumatra, Aceh, Riau, Jambi, West Sumatra and South Sumatra) and Java Island. Its stable of brands include Alhami, Santremie, Maitri and Alimi.

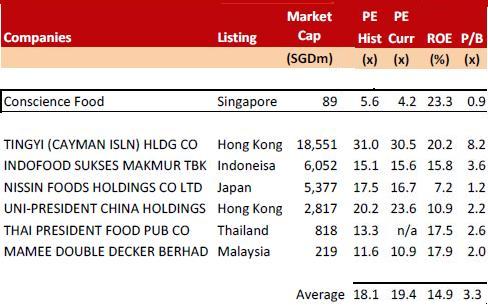

Growth led by product expansion.

CSF’s immediate growth driver is its expansion into cup noodle production in FY11F. It is also planning to establish or acquire a production facility around Jakarta to reduce reliance on its OEM suppliers, hence lowering production costs.

Low risks apart from ramp-up issues.

As a food manufacturing company, we see very little risks apart from natural disasters and contamination issues. The main risk to our earnings forecast is CSF’s inability to ramp up its upcoming capacity on time.

Target price of S$0.38 based on 7x FY11F earnings.

CSF is currently trading at 4.2x FY11F earnings, well below its peers’ average PE of 19.4x. We have valued CSF at S$0.38 based on 7x FY11F earnings, taking reference from its closest peer Mamee Double Decker.

Related story: CONSCIENCEFOOD made S$7.4 m in 1H net profit, up 14%

CIMB maintains ‘Buy’ call on Etika (45c) with 64-ct target price on horizontal integration via M&A

Analyst: Michelle Tan

Venturing into Indonesia to cross-sell products.

Etika recently acquired the maker and distributor of “Salam mie” and “Cintamie” instant noodles in Indonesia. The acquisition cost amounted to IDR24.2bn (S$3.5m). The group intends to use this as an avenue to broaden its distribution network for its key product – sweetened condensed milk. Management mentioned that they are building up the instant noodle factory in Jakarta and will be converting another factory in Surabaya into a condensed milk factory.

Other acquisitions to maximize distribution network.

The group also recently acquired other businesses that bake bread and ready to drink UHT milk to expand the reach of its own brand of sweetened condensed milk to countries such as Indonesia and Vietnam.

Stronger growth expected from completed acquisitions in FY10.

We expect revenue to jump significantly in FY11 once FY10’s completed acquisitions start to contribute to group revenue.

Maintain BUY and target price.

We maintain our BUY call for the stock and SOP target price of S$0.64. Our target price is pegged to a 10% discount to our sum-of-parts price of RM1.48. We continue to like Etika for its

1) strong growth record;

2) high market share in the condensed milk business in Malaysia; and

3) increasing dividend yield trend.

Related story: ETIKA: Profit growth to come from milk sales and Vietnam foray