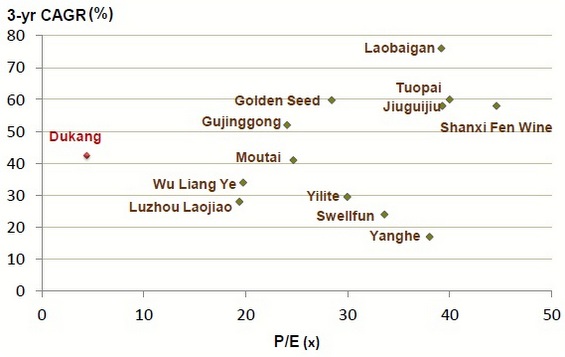

THE FALL IN the stock price of Dukang Distillers despite strong profit growth has displeased the company’s management, prompting it to consider moves to reassure the market.

Dukang is considering paying a dividend (after its current financial year ends in June) for the first time since its listing on the Singapore Exchange in 2008, as well as buying back its shares, said Zhou Tao, its CEO.

He was speaking from his office in Henan during a teleconference on Monday afternoon with analysts and the media after the release of the company's 9M12 results, and was asked to comment on the fallen stock price.

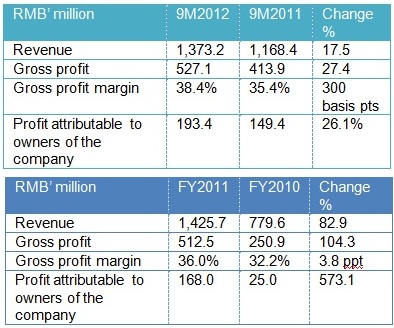

He pointed out that Dukang’s profit had headed north in FY11 ended June 2011 and in the 9 months ended 31 March 2012 (see tables below).

He said: “We need to beef up our interaction with investors – we need to invite them to visit our operations so they have a better idea of what we do.

"At the end of this month, a group of China funds and investors will be visiting us. We also will consider measures such as paying out dividends and buying back our shares.”

Dukang is a leading producer of baijiu in its home province of Henan, the most populous province in China.

The Group carries a broad range of baijiu products that are sold and marketed under two distinct brands, ‘Dukang’ (“杜康”) and ‘Siwu’ (“四五”).

Paying a dividend is, however, is no sure thing.

Despite a cash hoard of RMB583 million as at end-March 2012, Dukang considers that the cash could also be deployed to enable it to continue to grow fast, said Ngo Yit Sung, its corporate and IR Manager.

This can be achieved by increasing the number of fermentation pools and the production capacity of grain alcohol (more on this later)

Management is targeting to achieve RMB3-5 billion in sales over the next few years on a CAGR of 30% or more.

The market for baijiu is growing rapidly in China owing to population growth and rising disposable income. Demand for baijiu has been shown to be unaffected by economic down cycles. The market grew at CAGR of 30% in the 2007-2011 period.

A few other key takeaways from the telecon:

> Advertising & promotion expenses: This almost doubled to RMB111 million in 3Q12 as Dukang intensified its TV advertising, and bus and rooftop advertising in Henan.

In addition, for the first time, the Group also sponsored baijiu amounting to about RMB12.0 million for the “2012 Luoyang Peony Culture Festival”. These A&P expenses coincided with the peak 3Q sales period covering Chinese New Year.

Management said, on an annual basis, A&P would take up 10-12% of sales. It's relatively less than the 20-30% of sales that some other baijiu companies spend.

> Utilisation rates: Dukang's fermentation pools were fully utilised in 3Q12 -- a happy change from much lower rates of two years ago.

Dukang plans to create another 1,500 pools for which land and equipment would also have to be acquired. The total cost is estimated at RMB100 million.

"Do we go ahead and invest in our growth or do we use it to pay dividends which may benefit just short-term investors?" said Ngo Yit Sung, voicing the dilemma that high-growth companies typically face.

And there are other projects to invest in to boost the growth trajectory of Dukang, he added.

> Are prepayments to suppliers kept in an escrow account? UOB Kay Hian analyst Tan Jun Da asked this question.

CEO replied no, adding that the prepayments are necessary to secure the price and supply of raw materials for the year. "We are able to get back our pre-payments. There is no issue with it but we will consider starting an escrow account in the future."

Prepayments made up about 20% of the annual value of raw materials, and enable Dukang to save more on raw material price fluctuation than investing the money for interest in a bank account, said the CEO.

Dukang's Powerpoint presentation on its 1Q results is available on the SGX website.

Related stories:

The Edge hunts down 8 undervalued laggards that could catch up

DUKANG DISTILLERS: Rated 4 chillies out of 5 by Maybank Kim Eng