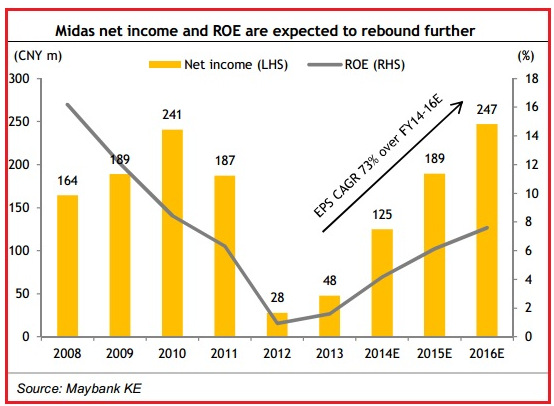

Maybank Kim Eng highlights Midas Holdings' 3-year EPS CAGR of 73%

Analyst: Wei Bin

Midas’s share price has retreated by 9.0% and underperformed the market by 10.7% in the past three months.

The stock currently trades at an undemanding valuation of 0.9x FY14E P/BV, which offers a safe entry point in our view.

Despite being a cyclical stock, we do not think 21.8x FY14E P/E is expensive, considering a three-year EPS CAGR of 73% over FY14E-16E.

The key earnings driver for Midas is operating leverage, as we expect HSR orders to bump up utilisation rate to 70% from around 50% currently.

We also expect ROE to improve to 3.8%/5.7%/7.1% in FY14E/15E/16E from 1.5% in FY13.

We believe Midas deserves a re-rating in view of the positive order win outlook and ROE expansion over the next three years.

Maintain BUY and TP of SGD0.75, pegged to 1.5x FY14E P/BV, which is at the lower end of its P/BV trading range in the last HSR cycle.

DBS Vickers says that buyers of Laguna Shores in Thailand are a good mix of Thai locals and foreigners, with Chinese and Russians being the main foreign investors. Its popularity is due to its location near the sea and its afforability – average pricing is < THB 10m (c. S$0.4m) for units under 800 sq ft. Image: Company

DBS Vickers says that buyers of Laguna Shores in Thailand are a good mix of Thai locals and foreigners, with Chinese and Russians being the main foreign investors. Its popularity is due to its location near the sea and its afforability – average pricing is < THB 10m (c. S$0.4m) for units under 800 sq ft. Image: CompanyDBS Vickers says Banyan Tree Holdings in Thailand will recover from 2H14

Analyst: Derek Tan, CA (left)

Analyst: Derek Tan, CA (left)While Banyan Tree (BTH) is expected to face some impact from the “Bangkok shutdown by anti-government protestors in 1Q14, we believe that the group will remain profitable given its

(i) heavier exposure in Phuket where performance of their resorts seem to be relatively shielded from the political woes in Bangkok,

(ii) diversified exposure across major hospitality markets of Maldives / Lijiang /Bintan where demand have continued to remain robust.

Positive take-ups in new property launches across Asia. The group’s new property projects – Laguna Shores and Laguna Park receive robust reception since their launch over 2012-2013 and the group is capitalization on this trend to other resort locations of Bintan and Penang.

We understand that sales continue to remain robust.

The group has unrecognized revenues of c.S$64.9m as of Dec’13 which might balloon up to c. S$130m, assuming that all units launched and its existing inventory of branded residences are sold.

The group has unrecognized revenues of c.S$64.9m as of Dec’13 which might balloon up to c. S$130m, assuming that all units launched and its existing inventory of branded residences are sold. We have not taken into account potential further property launches –i.e. Laguna Park (where the total development consists of c. 2,000 homes vs c. 15% of homes launched now), which the group intends to launch over 2014.

Maintain BUY, TPS$0.79. Looking ahead, with the worst of Thailand’s political crisis potentially behind us, we expect the operational performance of BTH group’s resorts to improve sequentially, while the group continues to unlock value from its vast landbank within Phuket through launching new property sales.

Our TP of S$0.79 and BUY call is maintained, based on SOTP valuation.